November 8, 2013

November 8, 2013

PBMs (or Pharmacy Benefit Managers) are big business. Just look at a few of the names and their place on the Fortune 500 list:

- Express Scripts

- CVS Caremark

- OptumRx (as part of United Healthcare)

- Prime Therapeutics

- Catamaran

- Aetna

- Cigna

- Humana

Not surprisingly, none of those are non-profits. There is real money being made here. It’s all part of the mark-up game in healthcare. The question of course is does the money being made justify the profits. For example, I’m happy to pay my banker lots of money as long as he’s earning me more than he’s making (and significantly more).

This is a complicated question. (see past posts on What’s Next, Why People Don’t Save With Mail, and Growing Mail Order) I’ve also presented on this topic several times in the past pointing out that the model needs to change, and re-iterating the fact that PBMs made a mistake by putting all their profits in the generic space. I’ve always said that disintermediation would happen by focusing on generics at mail which is where all the money was at Express Script (8 years ago). [People remind me that some of this has changed and is different across PBMs.]

The new Fortune article by Katherine Eban called “Painful Prescription” certains shows a dark story. It focuses exactly on one of these scenarios which is the gap between acquisition cost and client cost. The article talks about paying $26.91 for a drug but selling it to the client at $92.53. I’m always reminded of the fact that at one time we used to buy fluoxetine (generic Prozac) for about $0.015 per pill. On the flipside, we had brand drugs that we bought for more than we got reimbursed and lost money. It was strange model.

So, here’s my questions:

- Do you want transparency? If so, there are lots of “transparent PBMs” and many larger PBMs will do transparent deals. You can also follow the Caterpillar model. (Don’t forget that pharmacy represents less than 20% of your total healthcare spend so you can find yourself down the rabbit hole here trying to shave 2% of spend on 20% or 0.4% of your costs with a lot of effort.)

- Are you focused on anamolies like this one or average profits per Rx?

- Do you have the right plan design in place?

- Do you have a MAC (maximum allowable cost) list both at retail and mail order for generics?

- Are you getting the rebates and any admin fees from pharma for your claims passed through to you at the PBM?

- If you pay the PBM on a per Rx basis (i.e., no spread allowed), what are they doing to keep your drug costs down year over year (i.e., they have no more incentive to push down on suppliers)?

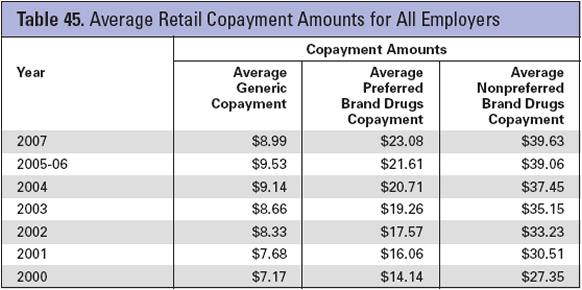

- Are you benchmarking your pricing? Look at reports from places like PBMI. For many smaller clients, I often wonder if the savings they find you is worth the costs.

I’m sure there’s more since I’ve been out of the industry for a few years, but while I don’t intend to be the defender of the industry, I do like to bring some balance to the conversation.