April 24, 2014

April 24, 2014

The CVS Caremark publication Insights 2014: Advancing The Science Of Pharmacy Care came out the other day. They took a different approach than the detailed trend report which Express Scripts put out. Their document is more of a white paper about “7 Sure Things”.

The 7 Sure Things are to help you know what to do with your pharmacy benefit and cover:

- Prescription trend is on the rise.

- Generics have peaked…and you’re going to feel the difference.

- Specialty drives trend. But do you know how much?

- Price is King…Not much of a surprise there.

- Money matters to members. Cost share does influence behavior.

- Adherence is the answer. No one said it was going to be easy.

- Past performance is no guarantee of future results.

If you’re managing a pharmacy program and you’re surprised by any of these, I would suggest you look for another job.

So, let’s drill down into the report to see what it shows us:

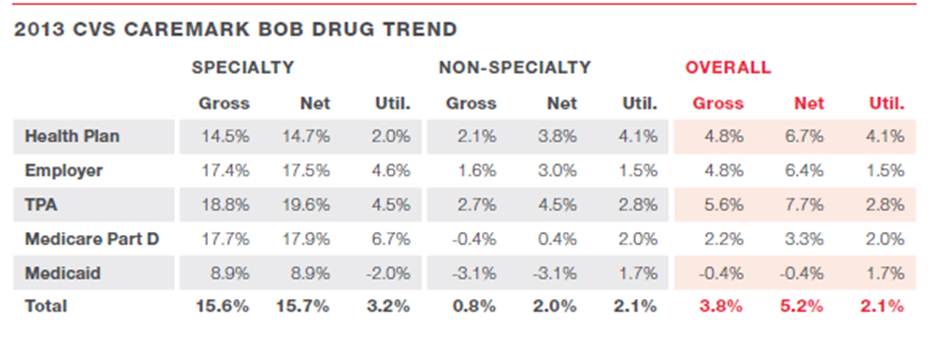

- Their trend numbers were:

o 0.8% for traditional (non-specialty) drugs

o 15.6% for specialty drugs (down from 18.3% in 2012)

o 3.8% overall

- While utilization was up 2.1%, the primary driver was price which increased 8.2%. These factors were mitigated by a 6.0% change in mix.

o They hint at an interesting question of whether utilization is growing due to an improving economy. (correlation or causality?)

- Their GDR (generic dispensing rate) was 81.4% in 2013. (I’d love their perspective on a maximum GDR since they say it’s peaked.)

- I like the chart below which shows trend with and without generics coming to market.

- Of course, specialty continues to be the real story in all the PBM reports.

- They claim that 53% of total specialty medication costs were paid under the medical benefit in 2012 which is in-line with most projections. (While they give some perspective on what to do here, this would be one thing I would have liked to see broken out in more detail as this is a critical area for PBMs which hasn’t been cracked yet.)

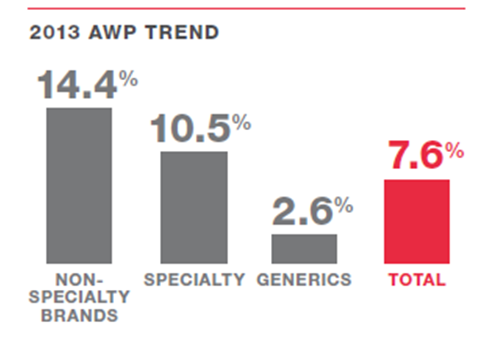

- They share the AWP trend broken out below and give some crazy examples of AWP price inflation (e.g., 573% for clomipramine) with some explanation for why this happens.

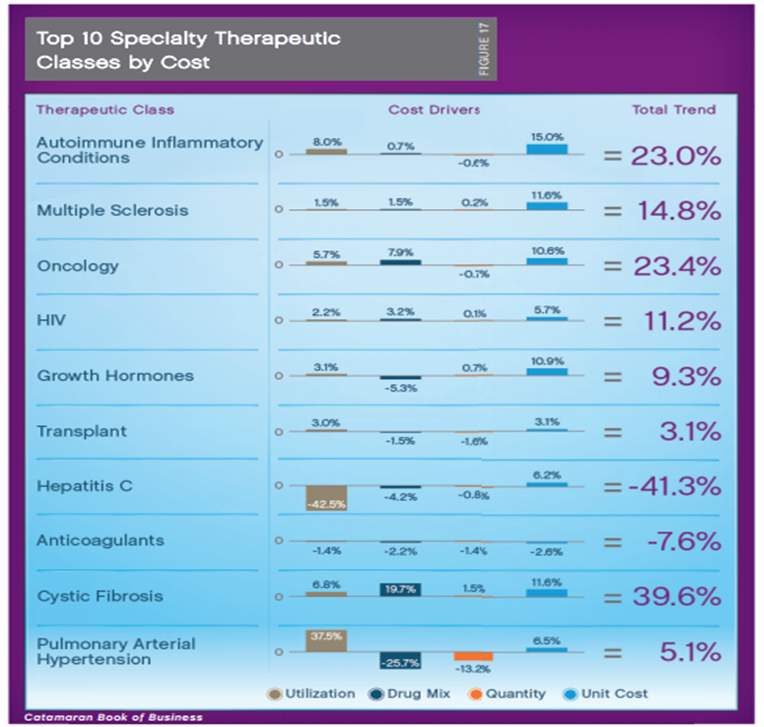

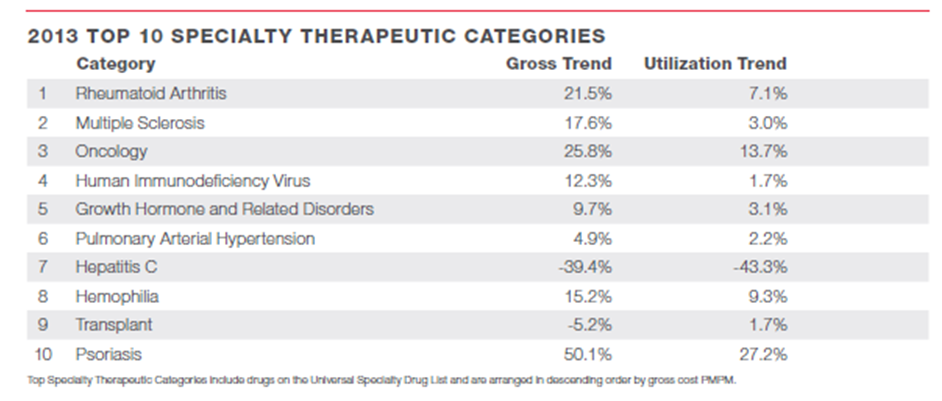

- Here were their top 10 specialty drug categories. The top 5 are the same as the CatamaranRx list, but the bottom 5 are in a different order.

- A scary statistic (in isolation) is that over the past 5 years patient out-of-pocket costs for prescriptions have climbed 250%. (But, I think their percentage of cost share has stayed the same. It would be interesting to show this in real dollars and compare this to both price and wage inflation just to hammer home the point.)

- They talk about CDHPs (consumer driven health plans) and how that is impacting utilization and cost. (These are often high deductible plans where consumers pay out of pocket until they reach a certain amount…which often really makes the point in early January to consumers. And, can lead to dissatisfaction when that prescription that was $30 in December is now $350 in January.)

- They talk about adherence, and they certainly have continued to publish a lot of studies in this space. (They also know have Dr. Will Shrank on their staff full-time after working with him for years. I think very highly of Will as one of the best adherence researchers in the country.)

- They give a real high level mention of some of their new efforts around adherence:

o Simpler labels

o Synchronizing refill dates

o Reminder devices

o Digital / mobile tools

- They also provide this nice summary of how costs go up and where the savings come from. (Of course, the challenge is in drug classes other than these three and getting clients to give you any credit for the productivity savings and also netting out the program costs.)

- On a scary note, they predict that Rx trends may jump back into the double digits for the next 4 years.

At the end, they give 5 sure strategies that clients should do.

- Double down on generics. (To me, this means – step therapies, formularies, setting copays right, mandatory generic programs, and generic substitution programs.)

- Look across benefits at specialty. (This is a key one as I mentioned above. You need to think through how specialty drugs are filled and billed under medical.)

- Tackle price. (They are focused on distribution channel here, but I’d also think about copay levels, plan design, and value-based programs.)

- Be strategic about cost share. (They are focused on how cost share affects adherence which is important, but only one component of an adherence strategy.)

- Keep the big picture in mind. (They allude to it here, but I think this is a key point that ultimately it’s about outcomes and prevention.)

Overall, this was certainly the easiest “trend report” to read. It tells a clear story which is probably great for the average client and would drive more discussion with your account manager.