I just finished reading the 2013 CatamaranRx Drug Trend Report (2014 Informed Trends: Moments of Opportunity) and wanted to share some of the things that caught my eye. (BTW – CatamaranRx was formed by the merger of SXC and CatalystRx.)

One of the early comments in the document caught my eye. While simple, it is still so true in healthcare.

“Bringing consistency through a national perspective on best practices, a “local” understanding of how health care is practiced and deep insights at the individual level, to promote the very best outcomes.”

- They did a good job of tackling the impact of healthcare reform on the PBM marketplace and why this creates more opportunities.

“The looming pharmacy demand is also driving the healthcare market toward expanded cost containment and coordinated care measures. Industry estimates are projecting more than 30 million new PBM customers as a result of the ACA. This influx of new customers will stimulate creative cost management paradigms and entice new entrants into the PBM sector.”

- 50% of the new drugs approved by the FDA in 2013 were specialty drugs. (reiterating the fact that specialty is really the focus of the PBM today in terms of opportunity to influence trend)

- 30% of the new drugs approved were oncology drugs. (similar to years past)

- Orphan drugs without competition were 2.6x more expensive than orphan drugs with competition. (not too surprising)

- They point out that no true biosimilar has been approved in the US (which I didn’t realize). They also point out that international experience is that biosimilars will save 10-15% not the 40% projected by the CBO.

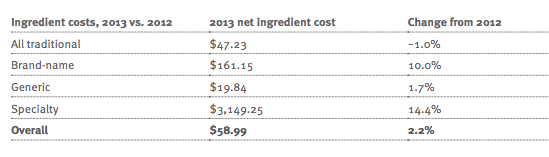

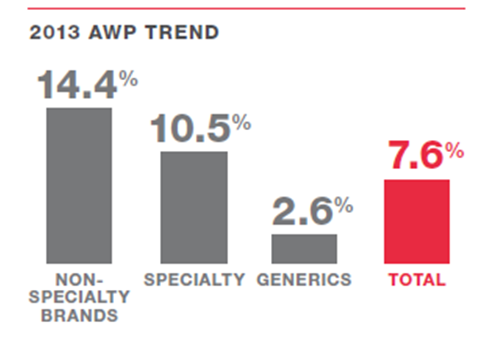

- They have nice clean charts around price inflation (deflation) for brand and generic drugs.

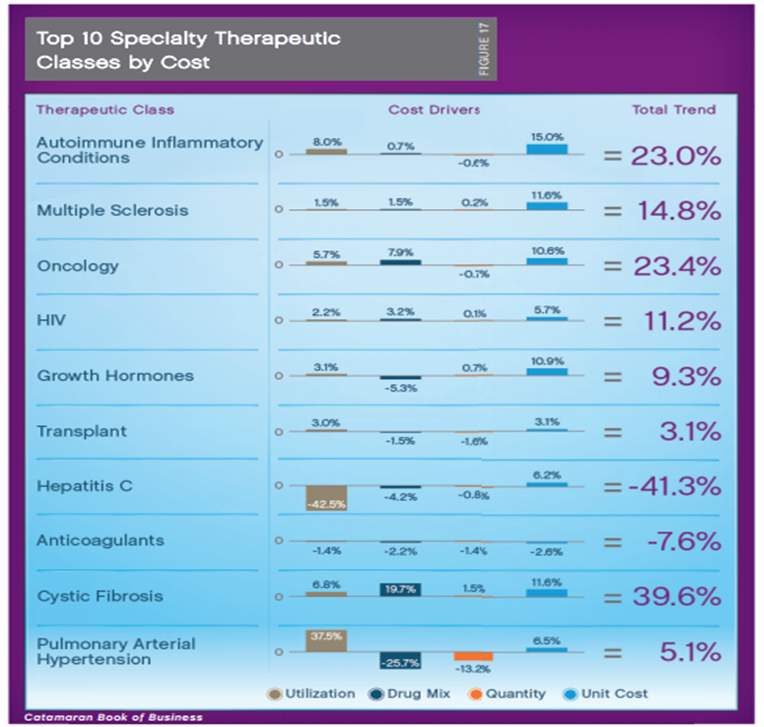

- The average cost of a specialty drug rose to $2,860 in their book-of-business.

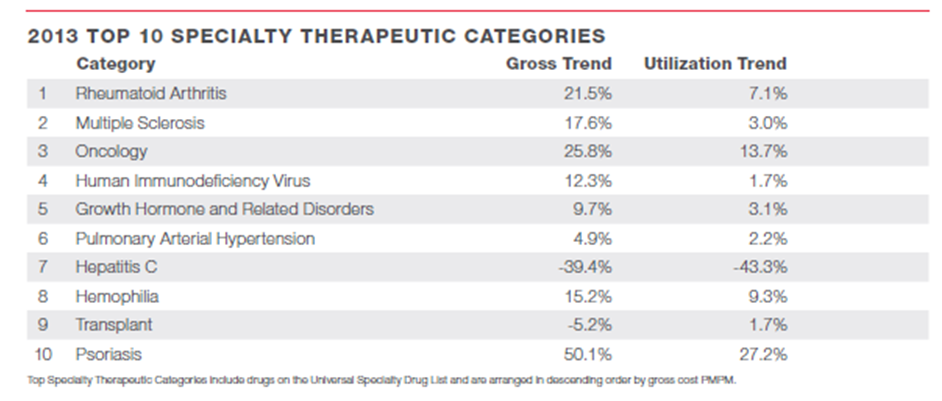

- The top 10 specialty drug classes represent 86% of specialty drug spend.

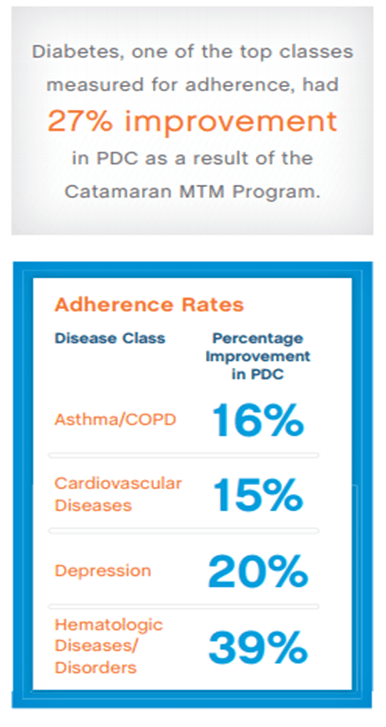

- The report talks about medication adherence using PDC (proportion of days covered). They show some good adherence rates in key classes (which always brings up questions about methodology).

o Over what time period?

o Is this all members prescribed an Rx?

o Is this all members with one Rx?

o What is the percentage of members with over 80% PDC (versus the average PDC)?

o (Note: These are the same questions for every PBM that shows you adherence numbers.)

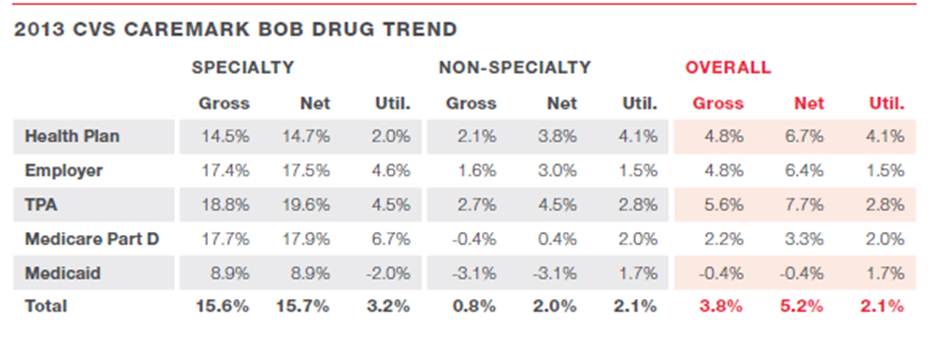

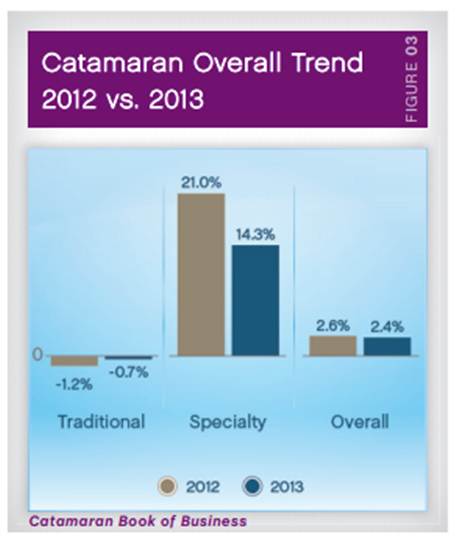

- Here’s their forecast for the next few years in terms of trend.

- They are projecting a generic fill rate of as high as 90% by the end of 2016!

- I like that they break out their highly managed clients to show they got an overall trend of -0.1% even though they had higher specialty trend driven by oncology. They shared a list of key things that those clients were doing:

o Member risk scoring and personalized interventions.

o Tailored clinical programs, including step therapy, quantity limits and prior authorization.

o Aggressive management of controlled drugs to reduce misuse and abuse.

o Formulary management tailored to address client-specific, high-cost medication classes.

o Exclusive specialty through BriovaRx, a high-touch, patient-centric model.

o Plan designs with copay differentials that promote cost-effective choices.

o Multi-channel communications that engage members in their healthcare.

- I was excited to see them dedicate a whole section talking about engagement.

o The need for the right message.

o The need for targeting algorithms.

o The need to vary channel based on preference.

- They share some details on their hospital discharge program which sounds right from a PBM perspective – focused on medication reconciliation and adherence. My key question would be understanding if they address the other risks of re-admission while they have the patient on the phone (i.e., treating the patient not the Rx and not the disease).

- I haven’t heard as much about MTM lately so it was nice to see them talk about it and see some results which seem really good.

Two miscellaneous comments here:

- This seems to be a much improved document than the one I reviewed years ago from SXC.

- My only challenge with the format was that it prints the two pages on one page in the PDF (but that could be user error).

June 19, 2014

June 19, 2014