July 24, 2014

July 24, 2014

In case you haven’t been tracking specialty drug costs for the past decade, the recent news with Gilead’s Sovaldi ($GILD) is finally making this topic a front page issue for everyone to be aware of. I think Dr. Brennan and Dr. Shrank’s viewpoint in JAMA this week did a good job of pointing that issue out. They make several points:

- Is this really an issue with Sovaldi or is this an issue with specialty drug prices?

- Would this really be an issue if it weren’t for the large patient population?

- Will this profit really continue or are they simply enjoying a small period of profitability before other products come to market?

- Based on QALY (quality adjusted life years) is this really quick comparable cost to other therapies?

If you haven’t paid attention, here’s a few articles on Sovaldi which did $5.7B in sales in the first half of 2014 and which Gilead claims has CURED 9,000 Hep C patients.

- Express Scripts Raises Pressure on Gilead

- Specialty Pharmacies Financial Win From Sovaldi

- A Poster Child For Predatory Pricing

- The Cost Of A Cure

But, don’t think of this as an isolated incident. Vertex has Kalydeco which is a $300,000 drug for a subset of Cystic Fibrosis patients. In general, I think this is where many people expected the large drug costs to be which is in orphan conditions or massively personalized drugs where there was a companion diagnostic or some other genetic marker to be used in prescribing the drug.

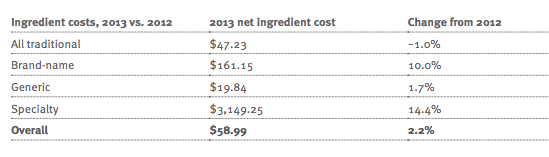

The rising costs of specialty medications has been a focus but has become the focus in the PBM and pharmacy world over the past few years. This has led to groups like the Campaign for Sustainable Rx Pricing. Here’s a few articles on the topic:

- AHIP Issue Brief

- Most Americans Worry About The Price Of Specialty Meds [even though they’ve never taken them]

- Prices Soaring on Specialty Meds

- Costly Cures

Of course, the one voice lost in all of this is that of the patient and the value of a cure to them. Many people don’t know they have Hepatitis C (HCV), but it can progress and lead to a liver transplant or even ESRD (end state renal disease) which are expensive. 15,000 people die each year in the US due to Hep C (see top reasons for death in the US). So, drugs like this can be literally and figuratively life savers. These can change the course of their life by actually curing a lifetime condition.

This topic of specialty drug pricing isn’t going away.

At the end of the day, I’m still left with several questions:

- What is the average weighted cost of a patient with chronic Hep C? Discounted to today’s dollars? Hard dollars and soft dollars? How does that compare to the cost of a cure?

- What’s the expected window of opportunity for Gilead? If they have to pay for the full cost of this drug in one year, that explains a lot. If they’re going to have a corner on the market for 10-years, that’s a different perspective. (Hard to know prospectively)

- For any condition, what’s the value of a cure? How is that value determined? (This is generally a new question for the industry.)

And, a few questions that won’t get answered soon, but that this issue highlights are:

- What is a reasonable ROI for pharma to keep investing in R&D?

- What can be done using technology to lower the costs of bringing a drug to market?

- For a life-saving treatment, are we ready to put a value on life and how will we do that?

- What percentage of R&D costs (and therefore relative costs per pill) should the US pay versus other countries?