April 10, 2014

April 10, 2014

I always enjoy reviewing the PBM Drug Trend Reports. Even though these past two years I’ve been focused more on the care management side of healthcare, I continue to see these two paths colliding in interesting ways in the near future.

Here’s my big takeaways from the report some of which you can get in their Executive Summary:

(I’d also encourage you to look at Adam Fein’s review…where he unfortunately beat me to the punch again.)

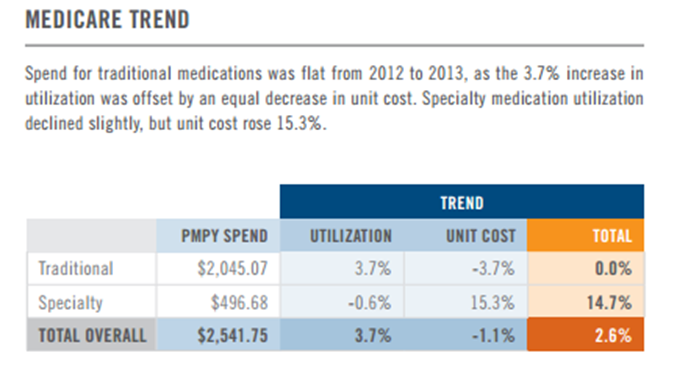

- Overall trend was 5.4% which they did a nice job of breaking out according to different lines of business.

- They also showed the breakout of trend comparing specialty drug trend versus traditional oral solid medications.

- Specialty trend was up 14.1% based on a 2.5% increase in utilization and an 11.6% increase in unit cost.

- A key point is that specialty now makes up 27.7% of the total drug spend for a payer (and that doesn’t even count the ~50% of specialty drugs billed under the medical benefit).

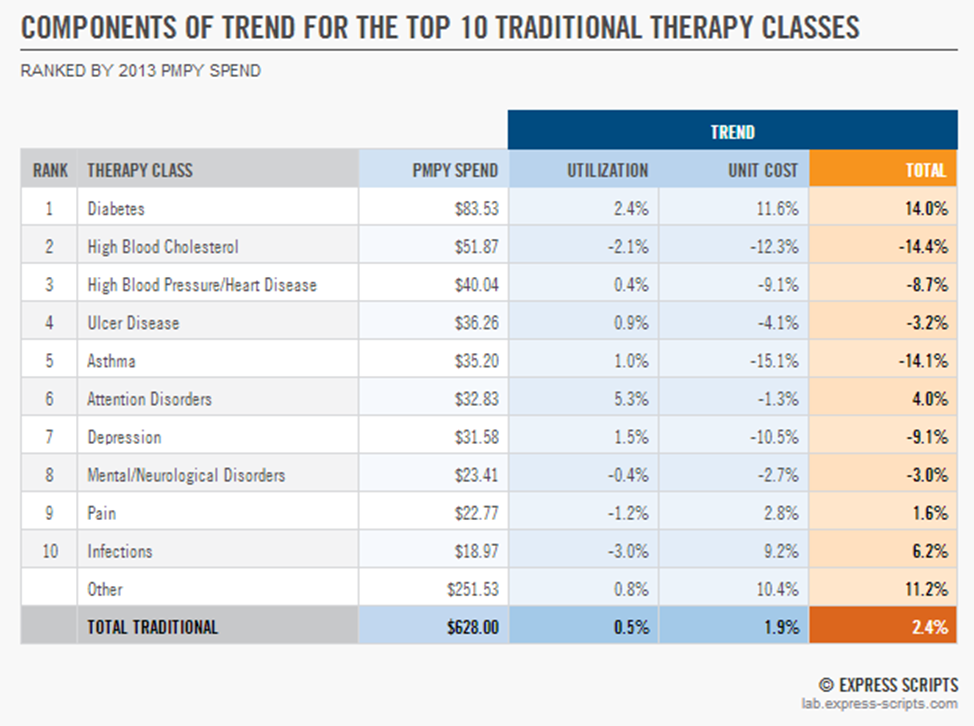

- Diabetes was the standout category within traditional drug classes with increased utilization and price increases. [Which isn’t surprising to those of us working on the clinical side that see huge innovation and investment in the diabetes area – Omada Health, Telcare, and Welldoc (for example).]

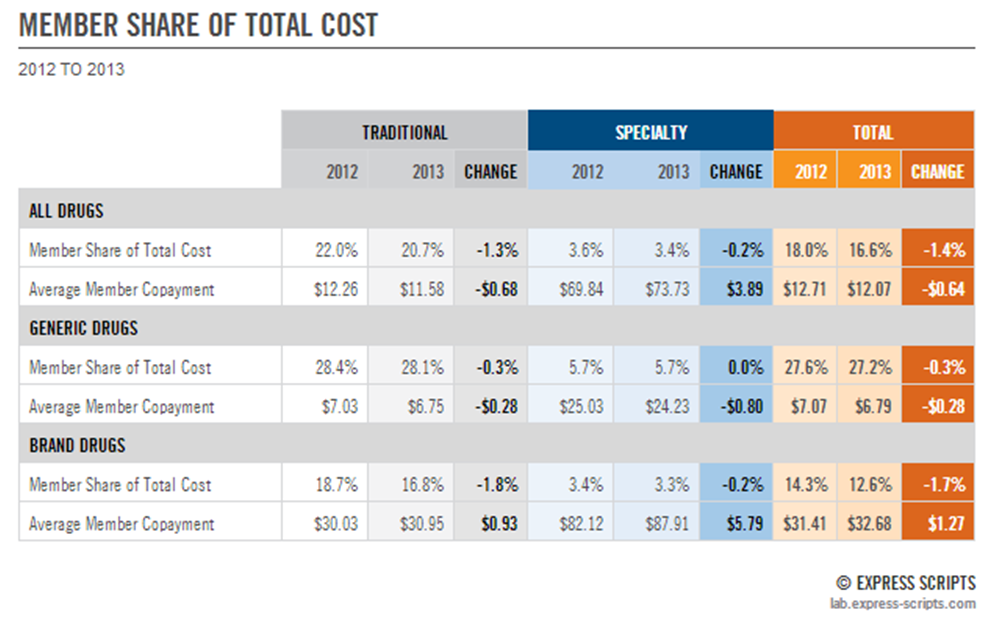

- While they make a key point with data that member cost share is going down and actual out-of-pocket costs are only going up marginally, I think it ignores the reality that consumers are feeling the pain of out-of-pocket spending more especially with all the High Deductible plans out there.

- They do reinforce their previous messaging around waste and also introduce their Health Decision ScienceTM approach. (I personally would have liked to see more on this. How is the blending of Consumerology and the Therapeutic Resource Centers impacting utilization, adherence, waste, clinical outcomes, patient satisfaction, or other key metrics?)

- As always, you can dig into their forecasts by drug class. I choose cancer as one area to look at. (While this is focused on the basics, I would have loved more about what’s going on around cancer. How are genetic tests impacting use? What about survivorship? How do Centers of Excellence affect outcomes, drug selection, pricing, and adherence?)

- On top of being able to drill down on Medicare and Medicaid, you can also look at a Worker’s Compensation specific version of the drug trends. This is interesting since that business is different than the traditional PBM market and is an area that Express Scripts has gone aggressively after in recent years.

- One thing I couldn’t find in the document (which is hard to read in the current format) is the average number of Rxs PMPM or PMPY which is just a good stat that I personally track.

- One note I will offer on methodology is the definition of specialty drugs. This could lead to some differences between PBMs as we try to compare their trend numbers. Here’s the definition Express Scripts offers:

“Specialty medications include injectable and noninjectable drugs that are typically used to treat chronic, complex conditions and may have one or more of the following qualities: frequent dosing adjustments or intensive clinical monitoring; intensive patient training and compliance assistance; limited distribution; and specialized handling or administration. – See more at: http://lab.express-scripts.com/drug-trend-report/appendix/methodology#sthash.dhJhFIZs.dpuf”