June 28, 2010

June 28, 2010

Of all the companies that might put out a restricted network whitepaper (PBMs, retail chains, consultants), I will admit that Wal-Mart is a surprise to me. It’s not that they haven’t been trying different strategies to increase market share – $4 generics, direct-to-employer contracting, but in general, I don’t see them doing a lot of marketing or selling in this space. They participate at one industry event, but their booth is very stark compared to other pharmacies.

But, that being said, the whitepaper makes the key points that anyone would make (i.e., I agree with the framing of the opportunity) with a slight twist of focusing on member savings versus payer savings.

Some of their key points from the whitepaper are:

- You should treat pharmacy negotiations like buying any widget. There is more supply than demand.

- Today’s model encourages all pharmacies to offer a rate that doesn’t get them kicked out of the network.

- Today’s model doesn’t encourage consumers to pick one pharmacy over another.

- There’s 5x more pharmacies than McDonald’s in the US…and no one would argue that it’s difficult to get a Big Mac.

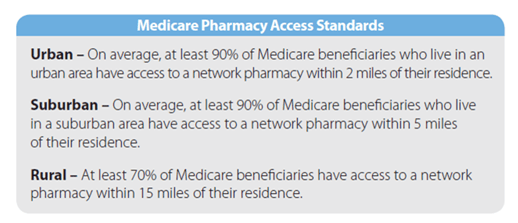

- They quote the Medicare pharmacy access standards to make the point about what access you can survive with. They reference an Express Scripts analysis that says the Medicare access standard can be achieved with a national network of less than 20,000 retail pharmacies (compared to the 60,000 in most networks).

While limited retail networks are not a new concept, they haven’t been widely adopted historically (<10% of clients). PBMs have always offered this type of plan design to payers – “If you remove a few chains from your network, you’ll get a lower rate from the other chains in return for increased marketshare.”

With the integration of CVS Caremark and their offer of Maintenance Choice, we’ve obviously seen the focus on this increase. And, the recent public negotiations with Walgreens highlighted that this is seen as a viable model for the future.

The question now is whether this will accelerate adoption of some type of limited network. If it goes forward, there are lots of questions to answer:

- How small will the network be – regionally, nationally?

- Who do you build the network around – CVS, Walgreens?

- What does this mean for mail order?

- What rates do the retailers have to match to participate?

- Does it include 90-day?

- Does the network start to look like a formulary where you have preferred pharmacies at one copay and non-preferred at another copay or is it either in-network or out-of-network?

- Does this increase or decrease power for the independents that have to be in certain places?

- Will anyone really test the national access standards and go to a 20,000 store network?

- What will consumers say and do?

- Does this accelerate adoption of cash cards and cash business for generics?

But, again, I struggle to see Wal-Mart as the chain that you build around unless the whitepaper is a thinly veiled attempt to push the direct-to-employer model (i.e., Caterpillar) which has saved the employer lots of money, but isn’t a simple to implement program (IMHO).

Here are some marketshare numbers for Walgreens, CVS, Rite-Aid, and Wal-Mart for the top 30 MSAs. Only 9 of those markets have Wal-Mart share above 10% and none are higher than 14%. For the other three, you have markets where they have a much higher concentration around which you can build.

Someone was asking me the other day if I saw the PBMs essentially partnering up. I’m not sure I do since there are markets where you would want to build a limited network with Walgreens and markets where you would want to build a limited network with CVS. At least for now, I don’t see Medco and Express Scripts just picking one dance partner although they might just based on who’s willing to play with them.

The other thing that becomes important here (tying this back to my Silverlink work) is communications. You have to identify who will be affected in moving to a limited network. You have to communicate with those people and help get them to the preferred pharmacy. You have to help them understand why you are doing this (savings) and WIIFM (what’s in it for me).

It creates some great dialog between the head of benefits and the CFO. We can save $X…BUT we will have to ask Y% of our employees and their families. Will they care? Do they know their pharmacist (unlikely)? Will it be an issue of convenience? Will they complain (of course…change is hard)? Will they ultimately care (unlikely as most disruption becomes accepted after 3-6 months)?

George,

As an independent community pharmacist, involved in this battle day after day, I appreciate your insights. I did struggle with one of the questions you posed at the end, “Do they know their pharmacist (unlikely)?” That is where we strive to separate ourselves in the market place. Personalized service, resulting in better outcomes, will untimately save healthcare dollars. That is if we are able to survive the predatory price schemes of the PBM’s as they attempt to put us out of business. Please write of call, I’d love to share our side of the story. Thanks

Phil – Thanks for your comment. I’ll send you an e-mail. I agree that the personal pharmacy interaction SHOULD be a differentiating point. The reality is that people do know their pharmacist more in a community pharmacy (especially in a rural location). But, is that enough? Can you survive on that? Can you charge a premium?

I saw an interesting statistic this morning in the USA Today from an AMEX survey that said that people are willing to pay 9% more for better service. Could the indpendent pharmacies charge a premium for their use. A model more MDs are (will be) moving to.

The other challenge is the managed care sees the savings from the healthcare spend (i.e., less hospitalizations). It doesn’t affect the PBMs at all. There needs to be a strategy for providing and getting reimbursed for cognitive services (i.e., consultation). Unfortunately, it doesn’t happen today which makes pharmacy more of a processing service and therefore a cost-driven industry.

With growing consolidation taking place in retail pharmacy space, Walmart is banking on cost increases resulting from oligopoly. After all, they know a thing or two about that. But 600,000 pharmacies in the U.S. equals to 1 pharmacy for 5000 people, which is not out of line, and the percentage of revenue from which an average retail pharmacy derives from drug sale hasn’t budged in years. Of course, one has to look at other numbers like: number of rx dispensed/pharmacist and the average dispensing cost/rx to get fuller picture of whether there is inefficiency brewing.

I have a tendency to believe that these retail chains are simply riding the growing trend of increase Rx usage, and are not contributing significantly to the cost problem that warrants employers to go to “access-based” plan design.

[GVA – Correction…there are about 60,000 pharmacies in the US.]

George,

Good points about geography, although I believe Walmart has 15-20% market share in many markets outside the top 30 MSAs.

As I mention in my original post on the white paper last week, Walmart will have trouble selling this concept given their particular geographic footprint and the general implementation difficulties. However, I do see momentum toward these models, even if we are only at the experimentation stage now.

In case your readers are curious, my Drug Channels post is here:

http://www.drugchannels.net/2010/06/exclusive-walmarts-pitch-for-smaller.html

Regards,

Adam