I originally wrote this for the Deloitte Center for Health Solution blog. It was then republished in the HealthCare Consumerism Outlook 2016 publication.

February 13, 2021

February 13, 2021  0 Comments

0 Comments

I originally wrote this for the Deloitte Center for Health Solution blog. It was then republished in the HealthCare Consumerism Outlook 2016 publication.

February 13, 2021 0 Comments

[Note: I’m republishing a few Deloitte blogs that they are no longer hosting as part of the new website.]

Originally Posted by George Van Antwerp on September 28, 2017

A flying car that conveniently folds into a briefcase never materialized, but the digital revolution now underway in pharmacy could lead to a reality not far from the futuristic world envisioned by The Jetsons cartoon series of the 1970s.

As an industry, health care is often seeking ways to pay for and reward value rather than volume. While pharmacy often lags behind medical in this area, discussions are starting to focus more on consumer engagement, patient satisfaction, clinical outcomes, and collaboration across the ecosystem (i.e., retail, mail, and specialty pharmacies, distributors, manufacturers, and pharmacy benefit managers (PBMs)). Rather than creating value through scale to drive price negotiations, three primary forces will likely push companies across the pharmacy ecosystem to transform their business models:

If we look to the future, will pharmacy companies be the delivery channel, the aggregator, the clinical care management company, the technology vendor or something very different? As pharmacy leaders ask themselves where they want to play and how they will win, defining the role of pharmacy within the health care ecosystem will likely be critical.

Technology: Imagine the following future scenario (all of which is in development).

As you start your day, your smart toilet detects abnormal sugar levels in your urine and alerts your physician. After a telehealth visit (from your couch) with an avatar of your physician, your physician gives you a prescription for a new medication. You fill your own prescription using a 3D printer. The generic drug is embedded with a smart chip that transmits clinical data back to the physician before dissolving in your stomach. The physician sends information about common side effects to your home monitoring system, which tracks your health and compliance. After a few days, your smart home recognizes you as you walk into the kitchen and asks how you are feeling. Your response about a rash correlates with a common side effect, and the monitoring system offers to schedule an appointment with your physician to determine if an alternative medication might be better.

While none of these technologies will see broad adoption any time soon, the pharmacy industry should consider investments now in preparation for the future. Such investments will likely help traditional players compete with start-ups and health-focused technology companies that will probably try to carve out the most profitable sectors (as we see in retail).

Pharmacy companies should be asking:

Consumerism: Today’s hypercompetitive marketplace often requires constant innovation and digitization. It commonly requires companies to look at their products and solutions through the eyes of the consumer, particularly as adoption of high-deductible health plans (HDHPs) continues to expand. One way to think about this is to follow the consumer journey. Here are four moments when consumers are often open to engagement:

| Open Enrollment | What is the best health plan for me given my conditions and prior medication use? How can I save money? What is the likely progression of my condition? |

| Diagnosis | What is wrong with me? What are my treatment options? How have other patients responded to this medication? What are the side effects? Is there a lower-cost medication? |

| Pharmacy Selection & Pick-up | Which pharmacy will save me the most money? Which pharmacy is most convenient? Where will I get the best service? What do I need to know about the drug and my condition? Will it interact with any food I eat, vitamins I take, or other medication? What is this prior authorization and why did I not know about it until I went to pick up my medication? |

| Ongoing Support & Management | What should I be doing to manage my condition? Why was my copayment so high? How can I see the status of my order in real-time through an app? How do I know if the medication is working? Am I better or do I have to keep taking the medication? |

Data: For many companies, it is still a challenge to integrate pharmacy and medical data. When you begin to look at lab data and unstructured data (e.g., patient reported outcomes, physician notes), the challenge can increase. At the same time, many technologies are creating new opportunities to leverage data and analytics to shift from reactive to proactive.

Data and analytics might help the pharmacy industry to:

Three drivers of change – technology, consumer, and data – will likely manifest themselves in different ways at different companies. As leaders think about business-model innovation and new product solutions using frameworks such as the Ten Types of Innovation or the Ambition Matrix, we will likely continue to see greater differentiation across the pharmacy market. I am excited about what this means for pharmaceutical manufacturers, wholesalers, PBMs, retail pharmacies, specialty pharmacies, and provider owned pharmacies.

This blog was first published in A view from the Center: Deloitte’s Life Sciences & Health Care Blog

February 13, 2021 0 Comments

[Note: I’m republishing a few Deloitte blogs that they are no longer hosting as part of the new website.]

Published Date : July 29, 2019

Author: Deloitte

Categories : Biopharma, Drug rebates, Health policy, Life sciences

On July 10, the White House abandoned efforts to eliminate safe-harbor protections for drug rebates in Medicare Part D and Medicaid managed care due to concerns that the change would lead to higher premiums for beneficiaries. (For background on this issue, see our previous blogs.) While the rebate issue is now off the table, pressure to reduce prescription drug costs is not. But rather than waiting for the next round of regulations, we believe the pharmaceutical industry should consider developing its own business models that address drug prices and demonstrate value.

Recall in January, the US Department of Health and Human Services (HHS) proposed eliminating safe-harbor protections for rebates beginning on January 1, 2020. The Congressional Budget Office (CBO) estimated the proposal would have increased Medicare spending by $170 billion and Medicaid spending by $7 billion over the next decade (see the May 7, 2019 Health Care Current). It also would have increased the premiums that Medicare beneficiaries would pay under Part D.

Who’s to blame for rising drug costs?

The Pharmaceutical Research and Manufacturers of America (PhRMA) said the decision not to eliminate safe-harbor protections for rebates was “a blow to seniors who could have paid less” for prescription drugs. America’s Health Insurance Plans (AHIP), however, said that drug manufacturers are solely responsible for setting drug prices and determining price increases, and could decide to reduce prices. In February, a group of biopharmaceutical executives told a Senate committee that eliminating safe-harbor protections—and shifting toward a value-based drug-pricing system—might be the key to reducing drug costs (see the March 5, 2019 Health Care Current). However, at a subsequent hearing, executives from five large PBMs suggested that increased competition among drug manufacturers could help to reduce drug costs.

At the heart of the debate is whether drug prices are artificially high because of the rebate system, or whether this system helps to bring drug prices down. In 2017, rebates and discounts offered by brand-name drug manufacturers reduced list prices by an average of 44 percent.1 Several PBMs have said they keep 5 percent or less of the rebates,2 which means the vast majority of rebate dollars are transferred to health plans, self-insured employers, and Part D plans to help reduce premiums. While some PBMs say they send 100 percent of rebate revenue to clients, they usually charge administrative fees to plan sponsors.

Four strategies for helping ensure market access

The average older American takes 4.5 prescription drugs, often to treat a chronic illness.3 Between 2012 and 2017, the average annual cost of four widely used prescription drugs increased about 58 percent, according to AARP. Even with the rebate proposal off the table, pressure to rein in price increases is likely to increase, which could push pharmaceutical companies to compete more directly on value. This might require a shift in strategy toward more robust evidence generation, the continued use and expansion of support services, and greater competition in value-based contracts. As we have suggested in previous posts, here are a few ideas pharmaceutical companies might consider:

Regulatory changes could accelerate use of value-based contracts

Over the past few years, we have seen an uptick in value-based contracts in several therapeutic categories. However, some barriers appear to be holding back widespread adoption. Some contracts have been abandoned before completion due to the amount of work required to operationalize them. While these contracts haven’t fully yet taken root, we expect the evolving regulatory environment could change that. The Deloitte Center for Health Solutions recently analyzed branded portfolios of the 19 largest biopharma companies (by revenue). From that list, we found 16 drugs that are (or were) included in a VBC.

While the rebate idea has been shelved, prescription drug costs will remain a top issue for the administration, Congress, and regulators as they advance policies outlined in the Blueprint to Lower Drug Prices and Reduce Out-of-Pocket Costs (see the January 8, 2019 My Take). Moreover, value-based contracting will continue to alter existing business models. The status quo is unlikely to remain and pharmaceutical companies and PBMs should prepare for change now rather than waiting for change to be mandated.

1 Adam J. Fein, Ph.D., Drug Channels Institute, April 24, 2018 (https://www.drugchannels.net/2018/04/the-gross-to-net-rebate-bubble-topped.html)

2 As a PBM and an Employer, We Know Rebates and Innovation Lower Drug Costs, Morning Consult, October 3, 2018 (https://morningconsult.com/opinions/as-a-pbm-and-an-employer-we-know-rebates-and-innovation-lower-drug-costs/)

3 Press release, April 4 2019, AARP (https://press.aarp.org/2019-4-4-Rx-Price-Watch-Report-Generic-Prescription-Drugs

February 13, 2021 0 Comments

[Note: I’m republishing a few Deloitte blogs that they are no longer hosting as part of the new website.]

Published Date : April 17, 2019

Author: Deloitte

Categories : Drug rebates, Health care providers, Health IT, Life sciences

Early this year, the US Department of Health and Human Services (HHS) proposed eliminating safe-harbor protections for the rebates drug manufacturers pay to pharmacy benefit managers (PBMs), Medicare Part D plans, and Medicaid managed care organizations. At the same time, HHS proposed two new safe-harbor protections for some point-of-sale (POS) price reductions on prescription drugs and certain PBM service fees.

The proposed rules, which are slated to go into effect on January 1, 2020, would not affect commercial health plans…at least not yet. On February 1, HHS Secretary Alex Azar urged Congress to pass its proposal “immediately” and to draft legislation that would extend it to the commercial drug market. In March, Sen. Mike Braun (R-Ind.) introduced the Drug Price Transparency Act (S. 657), which would extend the rebate prohibition to the commercial market.

With the rule prohibiting rebates in Part D still under review, and more than 25,000 comments submitted, Part D plans have to create their bids for CY2020, which are due in June. On April 4th, the US Centers for Medicare and Medicaid Services (CMS) announced it would let Part D plans test a new payment model that would reduce the risk of large gains or losses through risk corridors under a two-year demonstration. Additionally, CMS provided clarity that Part D plans should submit bids “in a form and manner that is consistent with the Anti-Kickback Statute law and regulations in effect as of the bid submission deadline, including, for the purposes of bid development, the treatment of manufacturer rebates per our existing rules and guidance related to Direct and Indirect Remuneration.” At the same time, during an April 9 hearing before the Senate Finance Committee, executives representing six large PBMs warned that eliminating rebates could lead to higher drug prices for seniors and argued that changing the business model by January 1, 2020, was not realistic.

While we have been tracking this issue closely over the past several months, it continues to evolve. In my October blog, The future of drug rebates: Are they to be or not to be?, I explained how pharmaceutical manufacturers use rebates when establishing list prices for their products. In November, my colleague Joe Coppola outlined some of the alternative models that could emerge if safe-harbor protections are eliminated. This third installment of our drug-rebate blog series examines how the proposed changes could affect various stakeholders.

At the heart of the debate is whether drug prices are artificially high because of the rebate system, or whether this system helps to bring drug prices down. Critics argue that rebates are to blame for high drug prices, while PBMs and health plans contend that rebates are an important tool in keeping rising drug costs in check. Others note that the rebate system existed and worked when plan designs were based on flat-dollar copayments. However, now that health plans often tie patient out-of-pocket costs (e.g., deductibles, coinsurance) to list prices for drugs, this might no longer be a practical solution.

Here’s what we know…

Regardless of how rebate reform rolls out, most stakeholders will be affected. At this point, there are many questions and few detailed answers. If HHS’s proposed rule is finalized and survives any legal challenges that arise, we can make several reasonable assumptions:

Here’s what we don’t know…

A big question surrounding HHS’s proposal is whether it will help achieve the administration’s goal of reducing list prices for prescription drugs…and at what cost? Here are a few questions we can’t answer until we have more information:

Stakeholders will likely have to prepare for change in different ways.

Here is how we think various stakeholders could be affected by the elimination of the drug-rebate model:

Regardless of the shape the final rule takes, and the timing of the implementation, we are already seeing various stakeholders distancing themselves from drug rebates. In a letter to Office of Management and Budget Director Mick Mulvaney last fall, former House Energy and Commerce Committee Chairman Greg Walden (R-Ore.), and former Senate Finance Committee Chairman Orrin Hatch (R-Utah) noted that possible changes to the existing rebate model “could ripple across the health care sector, altering a major sector of the U.S. economy that Americans depend upon for their health and well-being.” Depending on where you sit, this is either worrisome, long overdue, or the natural evolution of the market.

February 13, 2021 0 Comments

[Note: I’m republishing a few Deloitte blogs that they are no longer hosting as part of the new website.]

Published Date : October 18, 2018

Author: Deloitte

Categories : Biopharma, Drug rebates, Life sciences, Regulatory

Nearly half of all Americans (49 percent) have at least one prescription drug, and 12 percent of the population has five or more, according to 2017 data from the Centers for Drug Control and Prevention (CDC). In 2016, $329 billion was spent on prescription drugs—an increase of nearly 30 percent from 2010.1

With so much money at stake, drug pricing has become a front-page issue. But the sale of pharmaceuticals is based on a complex economic model that few people fully understand. It involves employers, health plans, pharmaceutical benefit managers (PBMs), pharmaceutical manufacturers, wholesalers, pharmacies, and the government.

As the administration looks for ways to reduce prescription drug prices, prescription drug rebates is one area that has come under scrutiny. Health and Human Services (HHS) Secretary Alex Azar recently said it was within his agency’s power to eliminate rebates on prescription drugs. A proposed rule from HHS, which could end or significantly alter rebates, is being reviewed at the Office of Management and Budget. This regulation could affect commercial health coverage and Medicare Part D, but might begin with an initial focus on Medicare.

How drug rebates work

Pharmaceutical manufacturers establish a list price for their products with an understanding that discounts and rebates will be used to reduce the list price employers or government programs actually pay. A clinical drug evaluation conducted by a PBM’s Pharmacy and Therapeutics (P&T) committee identifies which drugs have to be covered and which drugs are optional. Health plans and PBMs then consider rebates as they design their formulary (i.e., the preferred drug list used by health plans). This discussion considers the breadth of the formulary (i.e., number of drugs per therapeutic category), whether the formulary is open or closed, and the number of formulary tiers. Rebates typically increase as a formulary becomes more narrow (or closed) because it increases the likelihood that certain drugs will be prescribed.

In 2017, rebates and discounts offered by brand-name drug manufacturers reduced list prices by an average of 44 percent.2 Several PBMs have said they keep 5 percent or less of the rebates, which means the vast majority of rebate dollars are transferred to health plans, self-insured employers, and Part D plans to help reduce premiums. While some PBMs say they send 100 percent of rebate revenue to clients, they do charge plan sponsors administrative fees. PBMs also collect administrative fees from pharmaceutical manufacturers for managing the rebates. What is less clear is how consumers benefit from rebates. For example, do rebates translate to lower health insurance premiums for everyone versus directly benefiting only the patients who use the medications?

The administration views rebates as one lever that could have an impact on drug prices. At the heart of this debate is whether drug prices are artificially high because of the rebate system, or whether this system helps to bring drug prices down.

Antitrust litigation prompted drug-rebate model

Drug rebates became popular among PBMs after the antitrust litigation of the 1990s challenged the ability of drug manufacturers to offer up-front discounts. The courts determined such discounts ran afoul of antitrust law by favoring managed care providers over pharmacies. In response, drug manufacturers turned to rebates, which the courts indicated would be preferable.

Under current law, rebates are permissible because the anti-kickback statue—and implementing regulations—has a discount exception (also known as the safe harbor). The administration’s “blueprint” to reduce drug prices includes the removal of this safe-harbor protection of manufacturer rebates. The intent is to decrease out-of-pocket costs for consumers and reduce overall drug spending.

Over the past five years, the amount of rebates and discounts offered by pharmaceutical manufacturers has doubled to $153 billion in 2017, according to life sciences analytics firm IQVIA. This trend aligns with a growing number of high-cost specialty drugs and more aggressive cost-management tactics—such as closed formularies—among plan sponsors. Until the administration began focusing on drug costs, the gross-to-net bubble (i.e., the difference between the list price and the actual price paid after rebates) had shown no signs of decreasing.

The IQVIA data also indicates that while list drug prices have increased, net prices have remained relatively flat over the past five years. The higher list prices can lead to higher rebates, however one recent study suggested that there is no correlation.3 These higher list prices can result in bigger out-of-pocket costs for patients who have high-deductible health plans or coinsurance-based copayments, although they do help offset premium costs for all enrollees.

This issue of alignment, and how to contain drug costs, is at the heart of the issue. The ability to design formularies and negotiate rebates is a core value proposition for many PBMs. While the rebate model has existed in a bit of a black box for many years, from a business-to-business perspective, it has become less opaque (although not yet fully transparent). Consultants and sophisticated plan sponsors have increased their use of rebate audits and have called for greater transparency.

If the rebate model goes away, what will replace it?

Many groups have said it might be time to replace the rebate model. But what would replace it? Would all list prices need to be re-aligned to match today’s net prices or will a completely new model emerge? Will we see widespread adoption of value-based (or outcome-based) contracts between health plans, pharmaceutical manufacturers, and providers? At this point, there are no clear answers.

Several potential replacement models are being discussed that could take the place of rebates. A point-of-sale (POS) rebate model might be easiest to implement and could be an interim policy step. Under this model, the plan sponsor would have its PBM implement POS rebates so that members would pay the net cost of brand-name drugs. This could mean lower out-of-pocket costs for people who have high-deductible health plans or who are responsible for coinsurance. This would likely affect only a minority of members because rebates aren’t used for generic drugs, which make up almost 90 percent of all prescriptions filled in the US. It would not affect people who have flat-dollar copayments that aren’t tied to the net price of the drug (in a point-of-sale rebate scenario).

What can stakeholders expect if drug rebates are eliminated?

How would the list prices for drugs be affected if rebates are eliminated? Would pharmaceutical manufactures drop list prices down to the net price point, or would some alternative discounting program emerge? The other key discussion point is whether eliminating rebates will change the pricing trajectory and impact the industry’s economic model. If Average Wholesale Price (AWP) inflation slows, or reverses as a result, PBMs and other stakeholders that have some of their revenue streams tied to AWPs could need a strategy to replace lost revenue.

Eliminating rebates will not be like turning off a spigot. A PBM with a three-year contracting cycle, for example, might need a year or two to open and renegotiate thousands of contracts. Government bids, based on the existing system, are priced out almost nine months in advance. Without rebates, drug manufacturers will likely have to rethink their market-access approach and reevaluate their pricing strategies.

The loss of rebate revenue could cause plan sponsors to re-evaluate their pricing models, plan designs, and underwriting process. Without a new model to represent the current net-of-rebate cost for all drugs, consumers could see higher out-of-pocket costs, or more limited benefits to keep premiums from rising.

The drug-rebate model is extraordinarily complex, and people across the health care ecosystem are closely analyzing a variety of possible scenarios that could occur if that model changes or is eliminated. There are many questions that can’t yet be answered. Will rebates go away completely? How long will it take? Will the change be limited to Medicare? Will rebates continue to exist, but get shifted to the point of sale? Maybe the biggest question is…who wins and who loses? And can re-evaluating business models and potential financial vulnerability now help to create different winners?

We will begin to try to answer these and other questions in future blogs as we continue to dig into this issue and further evaluate the potential impact on all of the stakeholders in the health care ecosystem. Stay tuned.

1 Health Affairs, January 2018, “National Health Care Spending in 2016”

2 Adam J. Fein, Ph.D., Drug Channels Institute, April 24, 2018 (April https://www.drugchannels.net/2018/04/the-gross-to-net-rebate-bubble-topped.html)

3 https://www.pcmanet.org/new-data-rebates-are-unrelated-to-drugmakers-pricing-strategies/

February 13, 2021 0 Comments

[Note: I’m republishing a few Deloitte blogs that they are no longer hosting as part of the new website.]

Published Date : July 26, 2018

Author: Deloitte

Categories : Analytics, Health plans, Regulatory

First the good news. While we are in the midst of an opioid epidemic, large employers have seen prescription rates fall significantly since peaking in 2009. That year, 17.3 percent of covered employees or dependents had at least one opioid prescription. People who work for large employers are now using fewer prescription opioids.1 This is likely due to an increased focus—among health plans and clinicians—on limiting opioid prescriptions among patients who might be at risk for opioid dependence. There also is growing evidence that opioids aren’t appropriate for all patients or for every type of pain.

Now the bad news: Employers are spending nearly nine times more to treat opioid addiction and overdoses (prescription and illicit drug use) than they did 12 years ago—from $300 million in 2004 to $2.6 billion in 2016, according to the Kaiser Family Foundation. The average inpatient treatment cost for an opioid addiction topped $16,000 in 2016, according data from Kaiser. More than half of this spending is for the treatment of an employee’s dependent children. After a person first seeks formal help for an addiction, it can take as long as eight or nine years to achieve sustained recovery, according to a report from the Surgeon General.

And the ugly news: Opioids, both prescription and illicit, were involved in more than 42,000 deaths in 2016, according to the Centers for Disease Control and Prevention (CDC). That number is five times higher than in 1999. Moreover, emergency department visits for opioid overdoses increased 30 percent nationally between July 2016 and September 2017, according to the CDC.

Compared to people who do not have a substance-use disorder (SUD), people with SUDs incur higher health care costs and have a greater number of disability claims, miss more work days, and are more likely to be demoted or fired, according to the National Business Group on Health (NBGH). Along with direct medical costs, opioid addiction and treatment also impacts productivity, absenteeism, and recruiting, according to a recent NBGH survey of 62 large employers. One out of four employers say it has become difficult to find qualified workers who are not dependent on opioids.

Misuse and abuse of opioids is having a devastating impact on many employers and their workers and families.

Is workers compensation the canary in the coal mine?

Pain-related conditions affect 116 million adults in the U.S., according to the Institute of Medicine. This costs employers up to $635 billion in medical costs and lost productivity.2 Workers who are injured on or off the job could wind up becoming addicted to opioids that are prescribed to help manage their pain. While employers want to prevent addiction, the crackdown on prescribing is sometimes making it difficult for people to get access to opioids that they need to manage pain. Non-opioid therapies might not be as effective and could keep people off the job longer. What is the cost for employers when workers are unable to return to work either due to an injury or because of an opioid addiction? Moreover, some employees might choose not to seek help if they are worried about their job security. Employers want their employees to have effective pain-management options and don’t want them to seek illegal sources for drugs.

Workers’ compensation programs are often seen as employee benefits programs. They provide injured employees with a percentage of their salary until they are able to return to work. Given the volume of opioids being prescribed for work-related injuries, workers’ compensation insurers were some of the first organizations to recognize the critical role that physicians played in preventing opioid addiction.

Today, many workers’ compensation insurers are beginning to utilize advanced detection tools. Thanks to their unique position in the ecosystem—where they touch health care, consumers, and governments—they can effectively leverage state and federal guidelines, physician education, and advanced analytics to help prevent dependency and addiction.

Some industries have higher addiction rates

Industries where workers have physically demanding jobs, perform repetitive motions, or spend long stretches on their feet tend to have higher rates of opioid abuse. These industries include construction, automobile manufacturing, carpentry, and trucking. About 15 percent of people who work in the construction industry have engaged in illicit drug use, according to a lead commercial insurance carrier. The automobile manufacturing plants that produce more than 70 percent of US cars are in states that have seen significant increases in drug overdose deaths, according to the US Centers for Disease Control and Prevention. Recognizing an uptick in opioid abuse among truckers, the Department of Transportation added four prescription opioids to its mandatory drug-screening beginning on January 1, 2018.

What can employers do to address opioid use and abuse?

Given the costs associated with opioid abuse and misuse, employers might want to consider strategies that help prevent their at-risk employees from becoming addicted. But employers often need alternatives to treat pain among employees. They also need quality treatment for addiction. Strategies many employers are using to address this issue include:

Employers should also consider working closely with their health plans to develop solutions to curb opioid use and misuse. The Center for Health Solutions recently conducted research to find out what health plans and pharmacy benefit managers (PBMs) are doing to help address the opioid epidemic. Many health plans and PBMs have a stake in improving care outcomes, and they have key assets—especially data—that could be used for diagnosis and treatment.

Strategies that some health plans and PBMs are already using include:

Additionally, research indicates that the focus on opioid abuse is shifting to greater use of data and analytics to identify and engage those who might be at risk.3 Given the number of patients who use prescription opioids, and the ongoing threat from illicit drugs such as fentanyl, it can be to important shift from a fraud, waste, and abuse (FWA) mentality to a fraud, waste, abuse, and care approach.

An ecosystem approach is still needed

As we noted several years ago, tackling the opioid crisis requires coordination across health plans, PBMs, pharmacies, providers, employers, and many other constituents. This is a complex problem that goes beyond what any one group can influence.

At the same time, we cannot let the drop in new opioid prescriptions lull any of us into complacency. Systemic issues should be addressed from a policy perspective, including enabling data integration opportunities. And, given the need and risk of relapse, we likely need patient engagement strategies that effectively manage their risk over time and through treatment.1 Kaiser Family Foundation, April 2018: https://www.kff.org/health-costs/press-release/analysis-cost-of-treating-opioid-addiction-rose-rapidly-for-large-employers-as-the-number-of-prescriptions-has-declined/

2 National Center for Biotechnology Information, US National Library of Medicine: https://www.ncbi.nlm.nih.gov/books/NBK92521/

3 HealthIT Analytics: https://healthitanalytics.com/features/for-opioids-and-substance-abuse-big-data-analytics-is-just-the-beginning

February 15, 2016 0 Comments

I had the chance to share two new posts through other channels. For those of you that have followed me here, I wanted to share those with you.

I just posted a new blog about The Specialty Pharmacy Elephant on The Center for Health Solutions blog by Deloitte – http://blogs.deloitte.com/centerforhealthsolutions/the-specialty-pharmacy-elephant/.

I also used LinkedIn to share a post about The Pharmacy Marketplace in 2016.

February 17, 2015 0 Comments

For those of you that have followed me here, I thought I would share three things with you:

August 6, 2014 1 Comment

Cancer costs are expected to reach $174B in the US by 2020. Right now, it’s about 10-11% of total healthcare spend which makes it a big area of focus within the healthcare industry.

The question is how to manage this spend:

One of the challenges is the survival of the community oncology practice (see ASCO report) that is an issue that physicians have struggled with in other specialties. Over the past few years, we’ve seen continued consolidation of practices with many of them being acquired by hospitals and hospital systems.

In some cases, oncologists have seen a reduction in their income tied to a reduction in buy-and-bill and are looking to be employed in order to continue to maintain their incomes. They are one of the few medical professions that have seen a reduction in income recently. At the same time, this trend is also driven by hospitals taking advantage of the 340B pricing which allows them to generate approximately $1M in profit for every oncologist they employ. And, the complexity of oncology treatment also is prompting the need for a more comprehensive care model which requires a broad set of services which is sometimes difficult for a small practice to provide.

Of course, this shift in care from community oncology to hospitals is driving up costs without a demonstrated improvement in outcomes. This is driving a lot of payer focus and driving discussions of payment reform whether that’s in the form of ACOs, PCMHs, or bundled payments. United Healthcare recently released some data from one of their pilots.

This seems like another classic example of misalignment across the industry. Hospitals clearly see an opportunity to buy up more oncology practices while payers and others are going to push for reform around 340B and payment differences. Oncologists are struggling to continue providing care but replace the income they were making of buy-and-bill of specialty medications.

I’ve talked to a lot of people about this struggle. It doesn’t seem clear whether community oncologists are destined for extinction or will payers will find a way to enable them to survive. The other question is how things like teleoncology, tumor boards, big data, and the focus on prevention and survivorship will ultimately change the care delivery approach to oncology which may impact the role of the community oncologist in the future.

July 24, 2014 1 Comment

In case you haven’t been tracking specialty drug costs for the past decade, the recent news with Gilead’s Sovaldi ($GILD) is finally making this topic a front page issue for everyone to be aware of. I think Dr. Brennan and Dr. Shrank’s viewpoint in JAMA this week did a good job of pointing that issue out. They make several points:

If you haven’t paid attention, here’s a few articles on Sovaldi which did $5.7B in sales in the first half of 2014 and which Gilead claims has CURED 9,000 Hep C patients.

But, don’t think of this as an isolated incident. Vertex has Kalydeco which is a $300,000 drug for a subset of Cystic Fibrosis patients. In general, I think this is where many people expected the large drug costs to be which is in orphan conditions or massively personalized drugs where there was a companion diagnostic or some other genetic marker to be used in prescribing the drug.

The rising costs of specialty medications has been a focus but has become the focus in the PBM and pharmacy world over the past few years. This has led to groups like the Campaign for Sustainable Rx Pricing. Here’s a few articles on the topic:

Of course, the one voice lost in all of this is that of the patient and the value of a cure to them. Many people don’t know they have Hepatitis C (HCV), but it can progress and lead to a liver transplant or even ESRD (end state renal disease) which are expensive. 15,000 people die each year in the US due to Hep C (see top reasons for death in the US). So, drugs like this can be literally and figuratively life savers. These can change the course of their life by actually curing a lifetime condition.

This topic of specialty drug pricing isn’t going away.

At the end of the day, I’m still left with several questions:

And, a few questions that won’t get answered soon, but that this issue highlights are:

June 19, 2014 0 Comments

The Prime Therapeutics Drug Trend Report was released yesterday. Interestingly, they start out the report by making the point that what really should matter is net ingredient cost not trend. I’ve made the point before that trend isn’t a great number to focus on for many reasons. And, if you’re comparing trend numbers (which we all do), then you need to understand different methodologies. I think Adam Fein does a good job of summarizing that in his post. (BTW – This is a tough discussion to have especially when you’re getting spreadsheeted by consultants as part of an RFP.)

As comparisons, you can see my reviews of the other drug trend reports here:

Their report was short and to the point. Here’s some of the key data points:

Of course, anything anyone really cares about these days is specialty. Specialty represents only 0.4% of the scripts they fill but 20.5% of the spend for a commercial account. (They point out that this is much less as a percentage of scripts than other PBMs which have closer to 1% of their scripts classified as specialty…which could influence trend numbers.) The chart below shows how some of the things we all did around traditional drugs apply to specialty drugs.

And, they make a few predictions going forward:

June 17, 2014 0 Comments

For some people running mail order pharmacies, this analysis is no big surprise. They’re running off to their boss to show them that it’s not just their mail order facility, but it’s an industry issue. To others, they’re left scratching their head trying to figure out why this is. If mail order is where all the money is, what does this mean to them? (The historical PBM model put most profit in generics filled at mail order.)

Per a statistic mentioned in Drug Benefit News from Pembroke Consulting (and discussed here by Adam Fein), mail order prescriptions from 2012 to 2013 (excluding Medicare) dropped 9.2% while retail prescriptions jumped 2.7%. (This is not new news, but this is a big drop.)

I’ve talked about the issues and challenges of mail order many times:

At the end of the day, I simplify the mail order issue down to four major challenges:

Will mail order disappear? Of course not, but PBMs need to continue to either find ways to improve the consumer experience and make it better or they need to recognize the issues that exist and continue to diversify. And, with more 90-day prescriptions at retail for the same copay (i.e., CVS Caremark), this will continue to shift expectations.

May 27, 2014 1 Comment

When I saw this article and image in JAMA, I was really excited. It’s a good collection of structured and unstructured data sources. It reminded me of Dr. Harry Greenspun’s tweet from earlier today which points out why this new thinking is important.

People share more accurate #health & #lifestyle info through social media than with docs, what does that mean for…

— Harry Greenspun, MD (@harrygreenspun) May 27, 2014

But, it also made me think about this image and what was missing. The chart shows all the obvious data sources:

It even points out some of the newer sources of data:

But, I think they missed several that I think are important and relevant:

These things seem more relevant to me than fitness club memberships (which doesn’t actually mean you go to the fitness club) or ancestry.com data which isn’t very personalized (to the best of my knowledge).

In some cases, just simply understanding how consumers are using the healthcare system might be revealing and provide a perspective on their health literacy.

We’d like to think this was all coordinated (and sometimes scared into believing that it is), but the reality is that these data silos exist with limited ability to track a patient longitudinally and be sure that the patient is the same across data sources without a common, unique identifier.

April 24, 2014 2 Comments

The CVS Caremark publication Insights 2014: Advancing The Science Of Pharmacy Care came out the other day. They took a different approach than the detailed trend report which Express Scripts put out. Their document is more of a white paper about “7 Sure Things”.

The 7 Sure Things are to help you know what to do with your pharmacy benefit and cover:

If you’re managing a pharmacy program and you’re surprised by any of these, I would suggest you look for another job.

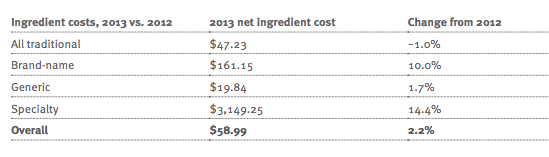

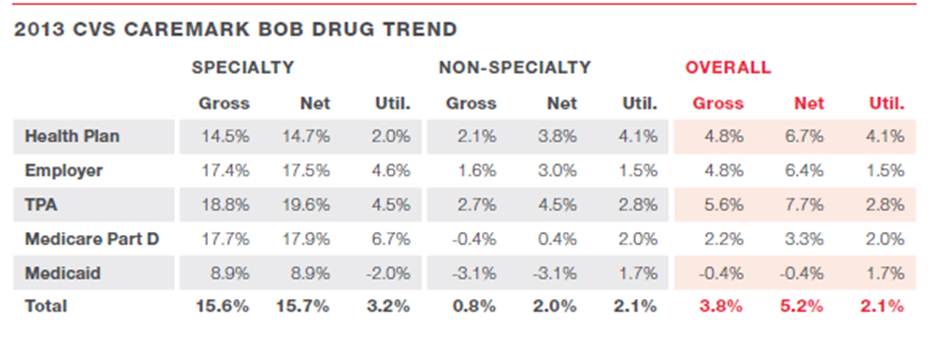

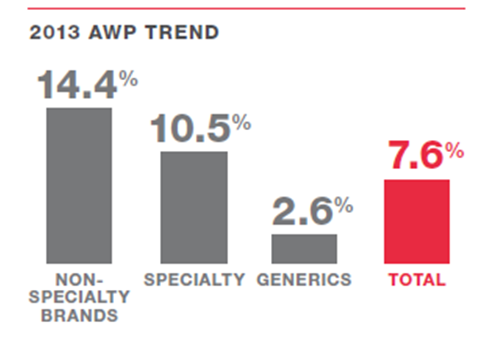

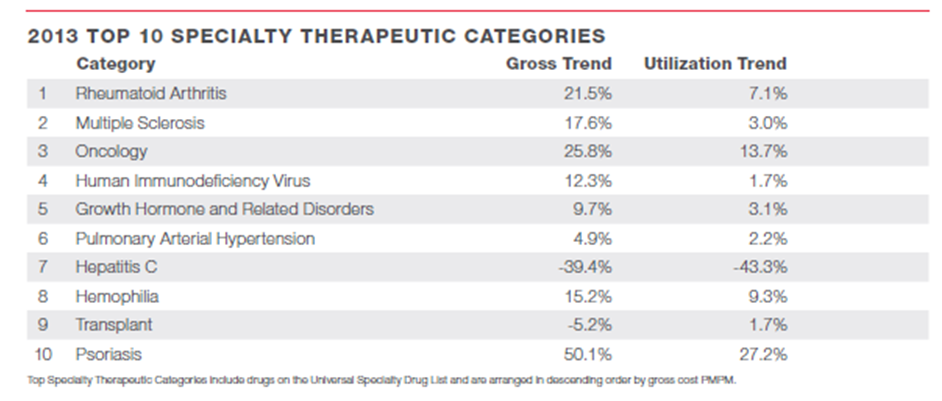

So, let’s drill down into the report to see what it shows us:

o 0.8% for traditional (non-specialty) drugs

o 15.6% for specialty drugs (down from 18.3% in 2012)

o 3.8% overall

o They hint at an interesting question of whether utilization is growing due to an improving economy. (correlation or causality?)

o Simpler labels

o Synchronizing refill dates

o Reminder devices

o Digital / mobile tools

At the end, they give 5 sure strategies that clients should do.

Overall, this was certainly the easiest “trend report” to read. It tells a clear story which is probably great for the average client and would drive more discussion with your account manager.

April 23, 2014 2 Comments

Every time I talk to a PBM, they want to convince me that they are unique. And, that is important to me (and should be to you). If they are simply driving generics, getting network discounts, and filling mail and specialty scripts, they’re clearly in a commodity space. It’s a race to the bottom, and they’re fighting very large companies – Express Scripts, CVS Caremark, and CatamaranRx. And, none of those companies are standing still. Of course, the other PBMs that are part of United Healthcare, Humana, and Kaiser are all looking at how they leverage the care assets and broader solution which they can bring to the client. (And, I’d put Prime Therapeutics somewhere in the middle based on their ownership by the Blues.)

But, as I’ve seen, value isn’t just about cost. That maybe one leg of the stool, but you need to improve outcomes and the consumer experience (i.e., The Triple Aim). With that in mind, I created a checklist of what I want to know to see if a PBM is really different.

This isn’t new…I’ve been talking about this for years. Here’s my whitepaper on this from 3 years ago.

And, here’s a presentation that I’ve given on this topic at several conferences.

April 23, 2014 3 Comments

I just finished reading the 2013 CatamaranRx Drug Trend Report (2014 Informed Trends: Moments of Opportunity) and wanted to share some of the things that caught my eye. (BTW – CatamaranRx was formed by the merger of SXC and CatalystRx.)

One of the early comments in the document caught my eye. While simple, it is still so true in healthcare.

“Bringing consistency through a national perspective on best practices, a “local” understanding of how health care is practiced and deep insights at the individual level, to promote the very best outcomes.”

“The looming pharmacy demand is also driving the healthcare market toward expanded cost containment and coordinated care measures. Industry estimates are projecting more than 30 million new PBM customers as a result of the ACA. This influx of new customers will stimulate creative cost management paradigms and entice new entrants into the PBM sector.”

o Over what time period?

o Is this all members prescribed an Rx?

o Is this all members with one Rx?

o What is the percentage of members with over 80% PDC (versus the average PDC)?

o (Note: These are the same questions for every PBM that shows you adherence numbers.)

o Member risk scoring and personalized interventions.

o Tailored clinical programs, including step therapy, quantity limits and prior authorization.

o Aggressive management of controlled drugs to reduce misuse and abuse.

o Formulary management tailored to address client-specific, high-cost medication classes.

o Exclusive specialty through BriovaRx, a high-touch, patient-centric model.

o Plan designs with copay differentials that promote cost-effective choices.

o Multi-channel communications that engage members in their healthcare.

o The need for the right message.

o The need for targeting algorithms.

o The need to vary channel based on preference.

Two miscellaneous comments here:

April 23, 2014 5 Comments

This is the “exciting” time of year when the PBM Drug Trend Reports come out. With the exception of last year, I’ve reviewed them every year. I reviewed the 2013 Express Scripts Drug Trend Report the other day, and I’ll try to do both the CVS Caremark and the CatamaranRx reports this week. The only one I’m still waiting to see is the Prime Therapeutics report. And, as far as I know, there aren’t any other PBMs that publish reports annually. (but please correct me if I’m wrong)

I’ll reiterate several points:

Here are the summaries from the 3 Drug Trend Reports showing the trend in PMPM costs based on traditional categories, specialty medications, and an overall trend.

January 23, 2014 10 Comments

It’s been a few years since I’ve worked on medication adherence solutions. It seems to have become a big focus again in the industry both with the Medicare Star Ratings program and with all the emphasis on waste.

As I started thinking about adherence, I thought it would be good to create a list of solutions and vendors. I couldn’t find one anywhere on the web. So, here’s my initial list of almost 100 companies.

I’ll make this a dynamic list so please comment or send me suggestions to add.

Here’s some old posts on adherence that I think are still relevant here:

I’ve divided the list of solutions and vendors into the following:

Devices

Mobile / Digital

Platform

Communications

Big Data

Tools / Enablers

Medicare focused

Condition specific

Packaging

Pharma

International (recommendations send to me without English sites)

What other companies am I missing? Send them to me directly or add them in the comments section here. Thanks.

January 6, 2014 0 Comments

A few weeks ago, as a follow-up to my discussion with Aetna about CarePass, I had a chance to talk with David Tripi from Janssen Healthcare Innovation about their new solution.

David is a founding partner at Janssen Healthcare Innovation where he is part of a multi-disciplinary group working toward the goal of propelling the company to become the leader in the healthcare solution business. Prior to the launch of the JHI team, David was with Johnson & Johnson for over 15 years.

“Janssen Healthcare Innovation (JHI), an entrepreneurial group within Janssen Research & Development, LLC, develops cutting-edge health solutions designed to modernize healthcare delivery, improve patient outcomes, and create a healthier world.” This is a 3-year old effort by Johnson & Johnson focused on integrated care businesses and enabling technologies. To support those, medication adherence and mobile are key areas.

One thing that David stressed is that they are platform agnostic and that their Care4Today Mobile Health Manager works as both an app and via SMS. Therefore, the 50% of the US that doesn’t have a smartphone can still use it. Additionally, it’s not a product or drug specific solution. You can use this even if you don’t use a J&J product.

Adherence is a huge challenge that everyone is aligned around, and everyone is trying to find solutions – plan design, incentives, apps, consumer engagement, framing, behavioral economics, and smart pill bottles (to name a few). So, what’s part of the Care4Today solution?

The idea of social health is important. We’ve talked about this for weight loss and smoking. But, with the expanded role of caregivers, can they play a key role in improving adherence? For example, if you respond that you didn’t take your pill and the response goes to your caregiver, will they call you? Will that follow-up motivate you? (Care4Family) Some prior research says yes.

A broader question might be about how to pick a caregiver or how to define it. Should it just be your family? Should it include your physician? What if you don’t have a support system? Could the healthcare companies or advocacy companies give you a “professional caregiver”? What about an avatar as a caregiver?

I asked about the incentive program that they included (Care4Charity). David pointed out that using apps isn’t fun (at least for most people) so they wanted to give a slight motivation. I questioned him on why $0.05 (which is the daily donation if you check in and take your meds). They did lots of research which showed that the amount didn’t really matter. So, this is an experiment to see if this extra feature of the program will nudge people to be more adherent. Or ultimately, it would be great to segment the population to understand who it was motivating for and for whom it didn’t matter.

One of the things I wondered about was how they were going to promote the app. Obviously, relationships with companies like Aetna and their CarePass program are one way, but with the tens of thousands of apps out there, how will people find it? David told me that they were going to initially focus on social media – Facebook, Twitter, and mommy blogs – to drive awareness. Next, they’re going to use pharma reps to discuss the app with physicians and pilot this strategy in HIV.

At the time, they’d had over 55,000 consumer downloads, and they’ve already gotten some initial feedback from physicians that like the fact that they’re offering solutions that aren’t branded to a specific pharmaceutical product. Some of those physicians are already offering it to patients. They expect this will be a big driver. They are now starting to talk with retail pharmacies about how to encourage consumer use. While my initial reaction was that this would be “competitive” with the Walgreens and CVS Caremark mobile solutions, they see collaboration opportunities especially with Walgreens and their open API.

Of course, I wondered about how the app was being used, but they don’t collect PII (personally identifiable information). In the future, they plan to offer an option for patients to opt-in to share information and create a clinic dashboard for physicians to see which patients are using it and providing them with data. And, with a new collaboration with HealthNet, consumers will be logging into the app with their HealthNet ID which will allow them to link up PII and PHI (protected health information).

So, what’s next…

Will it move the needle around adherence? It’s still too early to tell. But, it’s great to see pharma testing new strategies and working in new ways with payers to try to address this challenge.

November 29, 2013 2 Comments

With the new JD Powers survey, the gap between retail pharmacy satisfaction and mail order has widened. The average mail order satisfaction score was 797 for mail versus 837 (out of 1,000) for retail.

I think one key comment from Scott Hawkins, director of the healthcare practice at JD powers was:

“One of the key things we’ve seen in the data is that if someone is feels compelled to use a mail-order [pharmacy] their satisfaction score is going to be lower than someone who chooses to use it on their own.” (From Nov 2013 Employee Benefits News article by Andrea Davis)

If I was still at a PBM, I’d push to see the results broken out both ways so I could compare apples to apples the then say the drag was from clients choosing mandatory mail.

The rankings for mail order were:

Kaiser – 868

Humana – 845

Walgreens Mail – 812

OptumRx – 798

Prime Therapeutics – 794

Express Scripts – 783

Aetna – 778

Cigna – 771

Caremark – 760

The two I find the most interesting are Prime Therapeutics and OptumRx as both of them have moved their mail order services in house in the past few years and seem to be doing well with it. Aetna has outsourced their solution to Caremark and Cigna just recently outsourced their mail order to Catamaran which wasn’t on the list (but may be in the survey).

November 25, 2013 0 Comments

This is an interesting dilemma. At this point, I think everyone is pro e-prescribing even if it’s simply for the benefit of reducing errors. But, I think the original intent of the solutions were to do a lot more than reduce errors.

The hope was to improve adherence (which I think may have been too lofty). The idea was that e-prescribing would reduce the abandonment rate at the pharmacy. I’m not sure picking up a prescription is the same as taking a prescription. And, taking a prescription once isn’t the same as staying adherent over time.

Another hope was that the use of e-prescribing would drive formulary compliance and increase generic utilization. The idea was that putting this information in the hands of the prescriber would allow them to make more real-time decisions that were aligned with the consumer’s interests (i.e., lower out-of-pocket spend). The latest report doesn’t seem to support this at all. It also echos my prior posts about whether e-prescribing was aligned with pharma at all.

Fewer than half (47.5%) of the 200 PCPs polled said they have access to formulary information when e-prescribing, and fewer than a third said they have access to prior authorization (31.0%) or co-pay (29.5%) information. Among physicians with formulary information access, that information was available 61.1% of the time and was said to be accurate 68.6% of the time.

Physicians with an EMR (54.1%) were more likely to have access to formulary information than physicians without an EMR (29.6%). And differences were seen depending on the EHR vendor: Allscripts physicians (32.2%) were less likely to have access to this information than “All Other” software suppliers (60.5%), Epic physicians (62.5%) and eClinicalWorks (68.8%).

Another big effort that e-prescribing and integration with EMR was going to have was to push utilization management (UM) to the POP (point of prescribing) rather than having the pharmacy and the PBM dealing with it. I never really thought this would work. If the information isn’t there or they don’t trust the information, the prescriber isn’t going to want to deal with this. It’s already work that they let their staff handle and isn’t something they want to deal with during the patient encounter.

While e-prescribing is definitely here to stay and becoming the norm, the question is whether it’s creating simply a typed “clean” Rx to transmit electronically or whether it’s actually an intelligent process which will enable better care.

Given multiple studies and surveys recently about transparency in healthcare billing and the general push with Health Reform to drive to outcomes, I’m not sure the “dumb” system process can be a sustainable value proposition.

November 22, 2013 2 Comments

Last week, I noticed three recent reports that have come out about specialty pharmacy. I haven’t had a chance to really dig in to them , but I thought I’d pull out a few of the PR highlights and share the report links here.

The first report is from the Center for Healthcare Supply Chain Research and Health Strategies Group — “Specialty Pharmacy: Implications of Alternative Distribution Models” — which looks at how providers are using buy-and-bill and white bagging.

Karen J. Ribler, Executive Vice President and COO of the Center, notes, “Distributing specialty pharmaceuticals is complex; curbing costs is just one of the many facets of providing patient-centered healthcare. Site-of-care and day-of administration dosage requirements revealed themselves as determining factors for supporting the use of one method over another. A critical look at unintended consequences leads to our conclusion that Buy and Bill is, for the time being, the preferred model for practitioners of medium to large oncology clinics, but that could change as specialty treatments evolve.”

CVS Caremark just released their report Specialty Trend Management – Where To Go Next. In there, they say:

Infusions are increasingly being done in a hospital setting where the costs for both the drug and its administration can be the highest of all potential sites of care. For example, costs for a standard dose of a drug for rheumatoid arthritis can vary from $3,259 for the drug and $148 for administration when infused at the patient’s home to $5,393 for the drug and $425 for the administration when infused as an outpatient procedure at a hospital. In fact, the hospital setting is typically the least cost-effective site of care for infusions. (source)

As I’ve been doing lots of work lately in identifying and segmenting the population for Population Health Management, I found this chart interesting:

http://lab.express-scripts.com/prescription-drug-trends/specialty-drug-spending-to-jump-67-by-2015/

And, last month, Prime Therapeutics released a report on Specialty Pharmacy which I blogged about.

November 20, 2013 0 Comments

Is anyone really surprised here? We saw CVS Caremark make some changes a few years ago that caught everyone’s attention. (You can see a good list of 2013 and 2014 removals and options here for CVS Caremark.) This year, it’s Express Scripts (ESRX) who’s caught the attention of the press.

Why do this? I think Dr. Steve Miller did a great job of explaining it in a recent interview. The most interesting thing to come out of this was the possible link to copay cards.

Pharmalot: Where to from here?

Miller: We obviously have a long-term strategy. This has sent a loud message to the marketplace that we have got to preserve the benefit for patients and plan sponsors and do things to rein in costs. As there are more products in the marketplace that are interchangeable, we’ll do more to seek the best value for our members. This is just the beginning of a multi-step process over the next several years.

Will there be more to come? Of course. The PBMs have to make a significant show of lowering the number of formulary drugs especially in the oral solid (traditional Rx) space to make the point to the pharmaceutical manufacturers that they control market access. This is critical for them to create more opportunities in the specialty Rx space around rebates. (Here’s the 2014 Express Scripts exclusion list)

Additionally, this is a low risk strategy for several reasons:

November 8, 2013 0 Comments

PBMs (or Pharmacy Benefit Managers) are big business. Just look at a few of the names and their place on the Fortune 500 list:

Not surprisingly, none of those are non-profits. There is real money being made here. It’s all part of the mark-up game in healthcare. The question of course is does the money being made justify the profits. For example, I’m happy to pay my banker lots of money as long as he’s earning me more than he’s making (and significantly more).

This is a complicated question. (see past posts on What’s Next, Why People Don’t Save With Mail, and Growing Mail Order) I’ve also presented on this topic several times in the past pointing out that the model needs to change, and re-iterating the fact that PBMs made a mistake by putting all their profits in the generic space. I’ve always said that disintermediation would happen by focusing on generics at mail which is where all the money was at Express Script (8 years ago). [People remind me that some of this has changed and is different across PBMs.]

The new Fortune article by Katherine Eban called “Painful Prescription” certains shows a dark story. It focuses exactly on one of these scenarios which is the gap between acquisition cost and client cost. The article talks about paying $26.91 for a drug but selling it to the client at $92.53. I’m always reminded of the fact that at one time we used to buy fluoxetine (generic Prozac) for about $0.015 per pill. On the flipside, we had brand drugs that we bought for more than we got reimbursed and lost money. It was strange model.

So, here’s my questions:

I’m sure there’s more since I’ve been out of the industry for a few years, but while I don’t intend to be the defender of the industry, I do like to bring some balance to the conversation.

November 2, 2013 2 Comments

With several recent articles about $100,000 plus cancer drugs, I was reminded of a conversation I’ve had with several oncologists. We were discussing how to use advanced illness counseling from companies like Vital Decisions to help people and their families manage through a terminal diagnosis.

On the one hand, that seems like a conversation that a physician could / should have, but I’ve highlighted some research on this before. On the other hand, in a FFS (fee for service) world, there is an incentive to keep doing everything possible regardless of costs and how long it extends life. Will this change in a value based payment model? I’d like to believe it will. There is so much money spent on care in the last few months of life with limited extension of life and questionable impact on quality of life that this may become more relevant.

But, what struck me in my discussions is that the oncologists said that no one ever taught them how to “give up” on the patient. They see success in curing the patient or getting the cancer in remission. Is that success? Is it giving up to stop pumping them full of drugs with minimal value? Is there a rationale price for each day of extended life?

We typical think of healthcare as an endless bowl of funds, but what if it was limited? What if we couldn’t just keep printing money and raising the debt ceiling? Should that $200,000 be spent to get two weeks of life for a 90-year old patient in pain or should it go to feed a family and provide them with medical care for several years?

I’m not sure who wants to make those decisions but I think there will be a day when we need to think differently about some of the healthcare choices we make.

November 2, 2013 0 Comments

No one who works with consumers or who studies adherence should too surprised that people are different in how they fill their medications. I think companies are finally getting a better handle on longitudinal member records and ways of studying those patterns to determine how and when to intervene.

Our past behavior is always a great place to learn from about our future behavior but at the same time, people view different drugs and conditions differently. For example, I might be very likely to take my pain medication everyday since it’s a symptomatic condition versus my cholesterol medication since it’s an asymptotic condition. I also may take a different approach yo medications that have significant side effects.

At the same time, these data is well known so the quest for the “best” segmentation approach and behavior change model continues.

With that in mind, I finally got a chance to look at some research from September that researchers at CVS Caremark and Brigham and Women’s Hospital published in the journal Medical Care. They used trajectory modeling to follow statin users for 15 months and came up with six groups:

They also identified some characteristics associated with adherence:

Troyen A. Brennan, MD, MPH, Executive Vice President and Chief Medical Officer of CVS Caremark:

“The use of trajectory models could help us more accurately identify patients at risk for medication nonadherence so we can develop and implement targeted interventions to help them stay on their medications for chronic health conditions.”

October 19, 2013 1 Comment

I always tend to see the glass half full so when I see a problem then I often want to rush in and try to fix it. With that said, here are 10 things that I’ve thought about that I’d like to fix or see as big opportunities:

1. The healthcare experience. While this is the third leg of the Triple Aim, it often seems like the one that is so hard for healthcare companies to get. The system is so fragmented that the patient often is forgotten.

2. Device integration. While devices are better and integration is possible, there is still a huge lift to integrate my data into the typical clinical workflow. This is only going to get much worse with ubiquitous use of sensors and will be the limiting factor in the growth of the Quantified Self movement. (See my post on FitBit)

3. Intelligent phones. This is something that people carry everywhere. They often live life through the phone sometimes missing out on reality. The phone has tons of data as I’ve described before. We have to figure out how to tap into this in a less disruptive way.

4. Consumer preferences. I’m a big believer in preference-based marketing. But the question is how do I disclose my preferences, to whom, and are my preferences really the best way to get me to engage. What would be ideal is if we could find a way to scale down fMRI technology and allow us to disclose this information to key companies so they could get us to take actions that were in our best interest. (see old post on Buyology)

5. Benefits selection. I’ve picked the wrong benefits a few times. This drives me crazy. As I mentioned the other day, the technology to help with this exists and all the data which sits in EMRs and PHRs should allow us to fix this problem.

6. The role of retail pharmacy. This is one of my favorite topics. With more retail pharmacies than McDonalds and a huge problem of access, pharmacies could be the key turning point in influencing change in this country.

7. Caregiver empowerment. Anyone who cares for an adult and/or child knows how hard it is to be a caregiver and take care of their own needs. This becomes even harder with the people being geographically apart. With all the sensors and remote technology out there, I see this being a hot space in the next decade.

8. The smart house. As an architect, I’ve always dreamed of helping create the intelligent house where it knows what food you have. It manages your heat and light. It tracks your movements and could call for help if you fall. I see this being an opportunity to empower seniors to live at home longer.

9. Helping the disenfranchised. For years, we’ve all seen data showing that income can affect health. The question is how will we fix this. Coverage for all is certainly a critical step but that won’t fix it. We have a huge health literacy issue also. Ultimately, public health needs a program like we had to get people to wear seat belts. We need yo own our fate and change it before we end up like the humans in the movie Wall-e.

10. A Hispanic healthcare company in the US. With 16% of the US that speak Spanish, I’m shocked that I haven’t seen someone come out with a health and wellness company that is Hispanic centric in terms of the approach to improving care, engaging consumers, and providing support.

So, what would you like to solve?

October 18, 2013 1 Comment

The idea of healthcare costs and the need for healthcare transparency has become a front page issue. With the shift to consumer driven healthcare and high deductible plans, the average consumer is increasingly aware of what things cost. And companies like Change Healthcare provide tools to help consumers navigate this maze.

But, what I don’t hear many people discuss is the issue of middlemen and how this adds cost to the system. I’ve worked for several middlemen so I think I understand the model well. Of course, these companies make good (and true) arguments which is that they lower costs due to scale based efficiencies. But, healthcare is big business so everyone has to get paid somehow. Some of the “non-profits” make the most money.

Let’s look at prescription drugs:

– This begins with the manufacturer who adds the marketing and sales costs to the actual ingredient and packaging and shipping costs.

– The drug is then shipped to a wholesaler who stocks the drugs and ships them to pharmacies.

– The drugs are then sold by the pharmacy to the consumer and the pharmacy bills the payer.

– Assuming the payer isn’t the actual employer, the payer will then bill the employer.

So who all gets paid in this process:

– The manufacturer of the drug

– The advertising companies (they name the drug, they create the packaging, they create the ads)

– The marketing companies (they set up the websites, they create the mobile apps)

– The law firms (trademarks, patents)

– The sales companies (they hire and manage the pharma reps)

– The data company (the manage the Rx data to help target the reps)

– The shipping companies (transportation)

– The wholesaler

– The pharmacy

– The marketing and communication companies (refill programs, on the bag messaging)

– The technology companies (switch company, adjudication company)

– The recruiters (hiring, staffing)

– The PBM (contracting, rebating, customer service)

– The payer (adjudication, customer service, risk management)

– The broker (commission)

Still wonder why healthcare is expensive?

I wish I had an easy answer. A lot of these services are needed and it would cost more if the employers all had to do this themselves. There would be no scale. There would be no efficiencies.

This is certainly one argument for the efficiencies of a single payer system but I don’t think that’s very efficient IMHO.

October 7, 2013 0 Comments

It’s always exciting to be “right” in a prediction. When I spoke at the CBI conference a few weeks ago, one of the key points I made was that today’s healthcare consumer is overwhelmed with information. They get conflicting data. They don’t have enough time with their physicians. They are increasingly responsible for decisions and even with transparency, they don’t always know what to do. With that in mind, one of my suggestions was that retail pharmacies had a great opportunity to step in and be this information management source for consumers. (aka – The retailers can serve as the physical resource for the retailing of healthcare.)

With that in mind, I find the announcements by Walgreens and CVS very interesting.

From the CVS press release:

“Humana’s partnership with CVS/pharmacy reflects our proven and ongoing commitment to educate individuals and their families at the places they go when they have questions about their health,” said Roy A. Beveridge, MD, Humana’s Chief Medical Officer. “We’re working to ensure people develop a better understanding of how their health coverage can help them make better, and healthier, decisions.”

“Providing information about new health insurance coverage opportunities is in keeping with our purpose of helping people on their path to better health,” said Helena Foulkes, Executive Vice President and Chief Health Care Strategy and Marketing Officer for CVS Caremark. “We are pleased to combine our innovative suite of services and our new and existing relationships with organizations such as Humana to help patients understand and have access to information about insurance options in their community.

From the Walgreen’s press release:

Walgreens store personnel are directing individual customers who inquire to the GoHealth Marketplace, a resource where they can shop and compare health insurance plans, enroll and find other important tools and information. Consumers can access the GoHealth Marketplace online from www.walgreens.com/healthcarereform or via phone at 855-487-6969. Walgreens also is providing informational brochures and other materials in stores.

“As an accessible, community health care provider serving more than 6 million people each day, Walgreens can help connect those customers who may be considering new health insurance options with resources and information,” said Brad Fluegel, Walgreens senior vice president and chief strategy officer. “Our goal is to help ensure people fully understand the marketplace, and working with GoHealth, to provide personalized consultation from experts who can help them make informed decisions.”

In both cases, they may have addressed one of my questions about this strategy from my presentation which was how would they monetize this. I think it’s the right role, but I wasn’t sure how it would lead to revenue other than general revenue related to store traffic. I assume both of these have some “commission” or “referral fee” for traffic generated.

September 18, 2013 3 Comments

I’m excited to deliver my presentation on the topic about the retail pharmacy as the digital medical home tomorrow at the intersection of three CBI conferences – Point of Care Summit, Retail Strategy Summit, and Strategic Distribution Planning for Specialty Products. As always, I’m sharing my slides below via SlideShare, and I’ll set up some tweets to give you the cliff note version.

The key here IMHO is that retailers are best positioned to take advantage of this, but the key points are: