April 11, 2011

April 11, 2011

As I’ve talked about in the past, after working on the Express Scripts Drug Trend Report (recent copy here), I really enjoy getting the chance to read through them every year (see 2009 review or 2008 review). Over time, they’ve become less about the clinical side of the business and more about the programs used to engage the consumer with consolidated class specific data still included.

This year’s report is similar, but it is built around a new study that Express Scripts just completed with Harris Interactive. It comes to a rather surprising but interesting conclusion –

We discovered that the majority of people want to engage in the same behaviors plan sponsors seek to promote, but these desires often remain dormant. That is, there is a persistent intent–behavior gap. The key is structuring interventions that close the gap between what patients already want and what they actually do.

What’s the key point here? The point is that this says that consumers really want to move to generics and move to mail order, but they don’t do it. Is it that simple? I’d love to think so. And, for generics and mail order, I’m more likely to believe that inertia is a large factor. BUT, as I’ve talked about before, adherence has lots of complicating dimensions.

They focus on the gap between the physician and the optimal outcomes. This is certainly a major factor, but beyond consumer intent, there are issues of health literacy and physician beliefs that have to be addressed. Regardless, the point is correct…how do we engage and motivate consumers to change behavior especially if they are pre-disposed to change (when presented with the right facts).

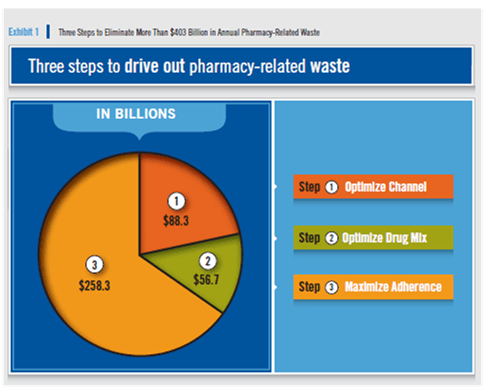

They did continue to build on last year’s focus on WASTE. They estimate that the waste in 2010 was over $403B as broken down below:

As adherence is a key issue here, they highlight the difference in adherence rates between retail pharmacy and mail pharmacy.

The focus of the report and the early press I’ve seen has been on the following chart. What it shows is some of the data from the Harris study saying that 82% of people would chose a generic (that are on a brand) and (depending on copay savings) 55-71% would chose retail.

One topic that I was glad was in the survey was limited networks. This is a topic everyone’s talking about from ReStat to Wal-Mart to Walgreens to CVS. Here’s what the research said with some explanation for what it means:

Of note is that about 40% said they would be willing to switch retail pharmacies to save their plan (or employer, or country) money. This fi gure is not as low as it fi rst appears because before a plan implements a more narrow retail network, a large fraction of members already use these pharmacies and therefore don’t have to switch pharmacies. It is not unusual, for example, for a client using a broad network to have 70% of prescriptions processed through pharmacies that are in the narrow network; members currently using these pharmacies do not have to make any changes. When a narrow network is implemented, if 40% of the users of the remaining 30% of prescriptions would willingly move to a lower-cost network pharmacy (as suggested by the survey), we estimate that the resulting overall market share within the narrow network would rise to 82% {70 % + (30% x 40%)}. (page 14 of the DTR)

All of this tees up their family of “Select” offerings (see Consumerology page) which builds on the success of Select Home Delivery and applies the concept of “Choice Architecture” from the book Nudge.

They talk about some of their work with adherence and their Adherence IndexSM. This metric is certainly one that has the industry’s attention as people wonder about the predictive value, how this is used, and how to craft solutions around such an index. My perception has been looking at studies like this one by Shrank and colleagues that past behavior remains the best predictor of future behavior, but I’m happy to be wrong.

So…what were the trend numbers?

- 1.4% in the traditional (non-specialty drugs)

- 19.6% in specialty

- 3.6% overall

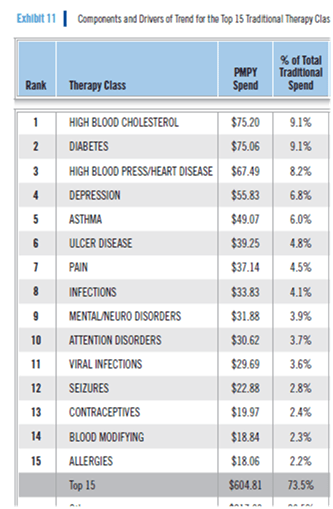

One of the other lists that I always find helpful to have is what are the top 15 drug classes and the PMPY spend.

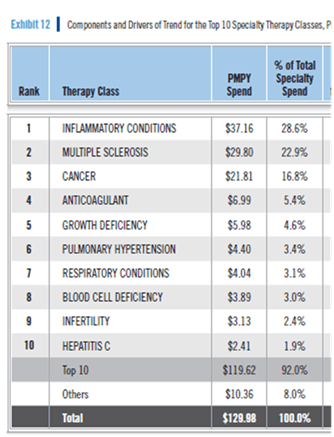

Of course, in today’s world, you really want to know this for specialty medications:

So, as always, I would recommend you read the report. Lots of great information in here. Interesting research. Good thoughts on consumer behavior and how to change it.

I think this week is their Outcomes conference which was always a good event.

In the beginning of the report, the company acknowledged obesity as a major driver of chronic diseases. This is an obvious fact, but many in our industry turn blind eye to it because obesity is so profitable. So a simple acknowledgement like this had my hopes up that ESRX had piloted an effective anti-obesity program with encouraging outcome to share in the report. Sadly, no such study or program was mentioned.

Who can blame them. With obesity being a powerful earnings-multiplier, especially in specialty business, there is no incentive to tackle this issue by for-profit organizations, at least not with our current payment and reimbursement structures.

Ultimately all the measures discussed in the report involve taking a slice of pie from someone else by labeling their slice as “waste”. There is no concrete idea for shrinking the size of the pie. Since mail-order and generic dispense rate have flattened out, all the low-hanging fruits are gone. So PBMs are having to resort to healthcare equivalence of extracting oil out of Canadian tar-sand.

As you all mentioned, adherence is a difficult issue to solve because there are so many variables, parties, and human emotion in play. I am very skeptical of the claim about $250 Billion “waste” caused by adherence, but even if we can reduce it by $20 billion/year, and surely that will involve monumental effort by the whole industry, that’s only about 1% saving of the total healthcare expenditure. 1%.

Bring obesity rate down to 1990 level, and third of us in the healthcare (more like healthbusiness) would be out of job, rather than spending our adult lives trying to figure out tactful ways to convince member that limited retail network is just as good, biosimilars are just as effective, and IVR is more convenient.

Does mail-order provide higher accuracy and adherence rate? Absolutely. Does it encourage some people to stay on medication longer than really necessary because it is so easy? Absolutely. Are people getting healthier? I’m not going to bet my money on it.

Going back to my oil metaphor, the day of drilling is over for healthcare. It’s tar sand. And tar sand extraction is expensive and dirty business. We need a healthcare equivalence of alternative energy. We really do.

Express Scripts Report Puts PBM Mail Order Profits Ahead of Patients, Health Plan Sponsors

The Express Scripts, Inc. (ESI) 2010 Drug Trend Report claims that the annual cost of “wasteful spending,” or what it considers suboptimal pharmacy-related behavior, is a staggering $403 billion. Unfortunately, the company’s recommendations for dealing with this problem are exactly backward.

Namely, Express Scripts’ top suggestion throughout the report is to shift patients from their community pharmacy to mail order, whether they like it or not. Mail order almost never produces the savings that its backers claim. But, even if one accepts the mail order cost estimates in ESI’s report, its mail order recommendation amounts to telling health plans to focus on 1.9 percent of this $403 billion in waste. (Per the report’s fine print, “$7.6 billion in savings would be achieved due to better unit pricing and lower dispensing fees in optimal channels” i.e., mail order.)

For many years, the Big 3 PBMs (ESI, CVS Caremark and Medco Health Solutions) have sought to increase their profits by convincing employers and other health plan sponsors to entice patients to switch to PBM-owned mail order by having the health plans pick-up 33 percent of the patient cost-sharing responsibility, or co-pay. (Of course, those costs don’t “disappear”; they are simply rolled into the insurance/PBM premiums paid by all patients and the plan sponsor.)

Despite this, mail order’s market share has been relatively flat in recent years. Common sense suggests three reasons for this: First, patients are satisfied with their community pharmacies. Second, mail order simply isn’t for everyone. And, third, because the employer is now absorbing the co-payment that was previously paid by the patent, mail order seldom delivers the promised savings to health plans.

To get around all this, the Express Scripts report uses creative “methodology” to assert that patients really prefer mail order, even though they still vote with their feet and wallets in favor of community pharmacies. There is no independent study to validate Express Scripts’ conclusion. In fact, this particular PBM’s mail order program was the least utilized among the Big 3 mail order services in 2010.

Express Scripts’ report claims that allowing consumers to bypass mail order and have their prescriptions filled at the pharmacy of their choice accounts for $88.3 billion of the $403 billion waste total. By contrast, in its 2009 Trend Report, ESI estimated this amount to be $6 billion. The change is simply sleight-of-hand to make mail order more attractive to employers, unless one believes that mail order costs decreased $80 billion in 12 months.

The two real savings drivers that amount to $395 billion of the $403 billion estimate – receive second billing in the report.

The first is “Non-Adherence,” or patients improperly taking their medication, estimated to cost between $258.3 and $308 billion. Like most PBMs that have selling mail order as their primary mission, Express Scripts equates medication possession with adherence. Of course, non-adherence is multi-variant with as many as 20 different drivers and non-possession of medication is but one.

The second is Drug Mix (i.e., using more generic drugs vs. brand names), estimated to cost between $56.7 and $87.7 billion. The irony here is that in 2010 Express Scripts mail order dispensed generic drugs just 60.2 percent of the time. This was dead last among the Big 3 PBMS and far off the 72.7 percent rate achieved by community pharmacists. Because of these numbers, it is unclear how moving more prescriptions from local pharmacies to Express Scripts mail order would promote higher generic utilization.

All of this is to point out that when it comes to 98 percent of the savings opportunities associated with the pharmacy benefit, Express Scripts needs to refocus its priorities on the things that really matter to patients and health plans rather than the bottom line of its mail order pharmacy.