November 17, 2010

November 17, 2010

I’m catching up on a few things this week. One of those is sharing my notes from the CVS Caremark Insights 2010 publication (their drug trend report). While this year’s report outlines all of the traditional things you would expect – trend, spend by condition, market conditions, generic pipeline, I really thought the exciting information was at the end where they really begin to stitch together the retail / PBM model. I’ve talked about why I believe in this model so strongly in the past (you can also see some of their executive’s comments here). And, I think my perceptions about the future of pharmacists create lots of opportunity for a combined entity. I also think they hint at some of the insights they gained from research around non-adherence and around abandonment which is important and creates a foundation for them around predictive modeling and focused interventions.

- I like that this year’s publication starts with a letter from Per Lofberg (the new President). He has brought them a renewed perspective on the PBM within the overall CVS Caremark enterprise which I think has been very helpful for them in this year’s sales cycle. [I personally haven’t met him yet, but I’ve heard a lot of good things about him.]

-

This introduction talks about:

- Generics, specialty, and genetic testing as key trends

- Controlling costs thru – plan design, clinical strategies, and negotiations with the manufacturers and retailers

- Executing flawlessly

- Improving outcomes

- I like the fact that they introduce the outcomes focus early on. I think that linking themselves to outcomes given their unique footprint (retail, PBM, clinic) is critical for long-term differentiation.

- Much like I see at Prime, CVS Caremark is a company that is blending its long-term team with some new leadership from outside the company and from the retail side of the business to drive innovation and change. I believe the clients and market has seen some of those changes already.

- A quarter of their clients maintained a gross trend of less than 3%.

- I found it interesting at the beginning of the document where they talk about the recession and macro-economy where they mention the effect that the COBRA subsidy had on health consumption.

- They say that their member contribution is 15.7% which seems really low to me, but that is pulled down by the Medicare average.

- As everyone has talked about, one of the big drivers of cost this past year was significant price inflation (9.7%) for brand drugs.

- Their generic dispensing rate (GDR) in Q1-2010 was 70.4%.

- Their average specialty trend was 11% with a best-in-class trend of 7.3% which seems really low.

- Not a big surprise, the top classes are similar to other PBMs with large commercial populations. Here’s the list of the top 10 categories:

- They mention later on their managed Medicaid lives (which I didn’t even know that they had). I think this should be a good growth area along with their Medicare Part D (PDP) lives.

- They introduce a new methodology which I like which looks at trend by group – employers, health plans, TPA, and Medicare. There are differences in each so being able to compare to a relevant peer group is valuable.

- They also talk about another change which is looking at book-of-business (BOB) which represent their top clients which represent 65% of total drug spend.

- Their average gross trend was 3.4% (or 2.4% if you exclude specialty).

- Digging into the best-in-class numbers is interesting. For example, for employers, 78.6% of their days supply was filled at preferred channel pricing (mail order or 90-day retail). I assume this is essentially for just maintenance drugs, but it seems really high (which is good) and is a new metric for me to think about.

- They talk about 77.7% of hypertensives (in employers) being optimally adherent (which I assumes means having and MPR > 80%). This seems pretty good, but I don’t have an industry number to compare to.

“With overall goals of reducing health care cost and improving member outcomes, health plan respondents in our 2010 benefit planning survey placed high value on proactive member outreach (93 percent), multi-channel access for members (87 percent) and opportunities for face-to-face consultation (73 percent)—all factors that can help keep members on prescribed therapies and satisfied.” (page 14)

- For each segment, they give the distribution of trend numbers. Here’s the one for health plans:

-

The best-in-class Medicare and Medicaid number for Generic Dispensing Rate are high and set a high goal:

- 78.2% Medicare Part D

- 86.8% Medicaid

Member retention is critical and involves a balance of copay levels, premiums and drug coverage as well as less tangible factors. Member satisfaction plays a significant role in loyalty and re-enrollment. High-performing plans focus on effective member communication and outreach as well as added-value services such as the CVS ExtraCare Health card.

- They talk about using a split generic tier design for Medicare to allow for different member copays for higher priced generics. I think this makes a lot of sense, but I don’t know all the details or member data and feedback to really understand how it plays out.

-

I’ve never spent much time on Managed Medicaid, but they give a few numbers here:

- Their average age is 17.6.

- The average PMPY spend is $288.

- Several times they use the term “evidence-based” which I really like. I recently was using that term to refer to communications and talking about how to leverage data to create “evidence-based” communications to consumers.

- They provide a nice 2-page summary of reform.

-

They put out a short list of recommendations:

- Prepare to take advantage of pending new generics; evaluate plan design and communication strategies for quick mobilization when new launches are pending. (This will be a big year for this with Lipitor.)

- Many specialty pipeline products are for orphan diseases and will have narrow indications; have plans in place to ensure appropriate utilization. (This will continue to be a bigger and bigger issue.)

- If you haven’t already done so, investigate the use of genetic testing to help guide treatment decisions. (Given their relationship with Generation Health this is an area that I expect to hear a lot more about in future Insights publications.)

- Newer, more expensive pharmaceuticals may offer little advantage over existing products in the class; consider step therapy or preferred product strategies. (I think Utilization Management (UM) activities like Step Therapy (ST) will be a continued focus for the next few years especially as biologics allow these “traditional” techniques to be applied to specialty.)

- Use wellness and preventive programs to identify people at high risk for chronic disease and help them lower their risk profile. (This is an area that I would have liked them to talk more about. As I’ve said many times, this is an opportunity for them to shine and differentiate.)

- Members with chronic disease who are non-adherent tend to have higher health care costs; evaluate your population’s adherence levels and the support you provide to help people stay adherent. (Differentiation in this area is a huge opportunity. I think they are doing some interesting work in this area as they’ve talked about in some recent press releases – Rx abandonment, barriers to diabetes care, US Airways program, and behavioral research.)

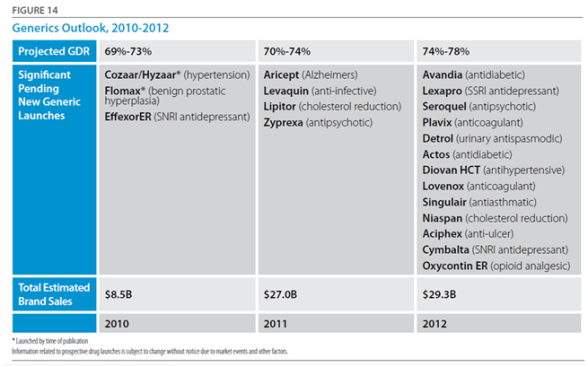

- They provide a forecast on trend for overall, non-specialty, and specialty. Here’s their forecast for the overall trend.

- They give a clear chart on the generic opportunity and likely impact on overall generic fill rates for 2010-2012.

- They go on to talk about specialty drugs which could be as much as 50% of the total spend by 2013…a scary prospect.

-

They have a good “state of the union” for specialty in the deck:

- As of January 2010, 57 percent of all late-stage pipeline drugs fell into the specialty area.

- 71 percent of applications for supplemental indications are for specialty products.

- The number of new specialty drugs approved in 2009 was more than double the number of 2008.

- Provenge, the first therapeutic vaccine—which utilizes the patient’s own DNA and stimulates the immune system to fight prostate cancer—was approved early in 2010.

- Potential approvals 2010-2012 include four new products for multiple sclerosis (all oral), three for hepatitis C, and three for cystic fibrosis.

- 18 of the products pending approval in 2010 target orphan diseases, which currently have few or no treatments.

- While health care reform legislation provides for a pathway for approval of biosimilars, it also mandates a 12-year minimum exclusivity period for brand innovators with the possibility of additional exclusivity in 12-year increments for the development of new uses.

- They then talk a little about pharmacogenomics (PGx). Again, I expect this to be a much bigger area in the future. It’s interesting. It’s changing rapidly. BUT, there is a huge education mountain for patients and MDs.

For a 1M member population, ~$12M is spent each year on 18 drugs that are administered to patients who do not respond and/or who are more likely to experience drug-induced medical complications.

-

I think some of the hidden gems begin on page 27 where they talk about their study on electronic prescribing:

- 22.1% never filled their first claim. (why – samples?)

- They found that those who had an eRx were most likely to fill than those with a paper Rx. (I personally would have bet on the other…i.e., that I have something physical in my hand that it would serve to remind me to go to the pharmacy.)

- Another study towards the end was on abandonment (which they recently released more information on). It showed that copay, income, and whether it was an NRx (new start on Rx) were predictors of abandonment.

- They also share work done around adherence focused on complexity of therapy – number of Rxs, number of MDs, number of pharmacies, and synchronization of refills. They talk about using this to score patients and predict risk of non-adherence. (I look forward to seeing more here since this seems very interesting especially in terms of focusing resources and developing a triage model.)

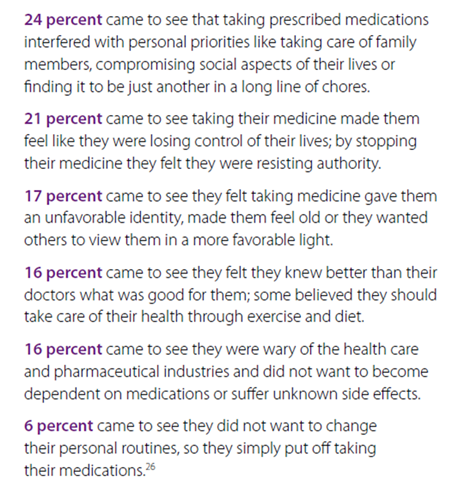

- They shared the results of a deep dive on reasons for abandonment of prescriptions. Being able to respond and position messaging around these reasons is important.

-

They share some of the work from their Pharmacy Advisor program:

- IVR messaging improved the odds of refills by up to 70.6% when members answered the phone.

- Early IVR refill reminders were 2x as effective for first fill persistency rates at mail as compared to reminders after refill due dates.

- Physician directed fax alerts about gaps in care nearly doubled gap closure rates.

- Pharmacist interventions were most effective at improving adherence.

- Members in VBID (value based insurance design) in which copays were lowered or eliminated were more likely to initiate therapy, less likely to discontinue therapy, and had better adherence.

“Diabetes is one of the most prevalent and expensive chronic diseases in the nation, costing the U.S. an estimated $174 billion a year,” said Troyen Brennan, MD, MPH, EVP and Chief Medical Officer of CVS Caremark. “The Pharmacy Advisor program improves clinical care because we are able to identify and address pharmacy-related care issues that if left unattended could result in disease progression and increased health care costs. We are also better able to engage the member in their care through multiple contact points, providing counsel that can improve adherence and help members optimize their pharmacy benefit and find the most cost effective options.” (quote from press release)

-

They talk about a pilot program they did in Polk County were patients signed a contract for care and was focused on diabetes care. It had some great results:

- Reduction in blood glucose levels from 52% under or equal 7% at the beginning to 72% after one year.

- 30% reduction in hospitalizations.

- 24% reduction in ER visits.

- Only 3.4% of enrolled members had poorly controlled diabetes (compared to national average of 29.4%).

- Improved patient care – identification of potential adverse events, streamlined medication regimens, and formulary support.

- (I personally would think this would get other plans (or PBMs) to partner with them on regional strategies where they have a strong retail presence.)

-

This also coincided with their announcements about their Pharmacy Advisor program which officially launches in January 2011. I’m very interested to see the uptake here which I would imagine will parallel the success of Maintenance Choice. This is a program which leverages their Consumer Engagement Engine (see image from last year’s report) and their retail presence to engage consumers.

Overall, it was an easy read without a lot of fluff. It cuts to the chase and gives you a good perspective on how they think. You begin to get a feel for what they are doing differently, but I imagine that you’ll continue to see a lot more research and case studies come out in the next year about some of the work they are doing.

(Note: In the sense of disclosure, CVS Caremark is a stock that I own.)

No comments yet... Be the first to leave a reply!