December 12, 2007

December 12, 2007

On 12/6/07, the WSJ had an article “Big Pharma Faces Grim Prognosis”. The manufacturers have been a good punching bag for a few years here as their creativity has slowed down (regardless of reality this is clearly the perception) and healthcare costs have become a front page issue. It is much easier to understand and compare drug prices than it is to look at provider costs. Now, with all the cost cutting at pharma, we will enter a new era.

On 12/6/07, the WSJ had an article “Big Pharma Faces Grim Prognosis”. The manufacturers have been a good punching bag for a few years here as their creativity has slowed down (regardless of reality this is clearly the perception) and healthcare costs have become a front page issue. It is much easier to understand and compare drug prices than it is to look at provider costs. Now, with all the cost cutting at pharma, we will enter a new era.

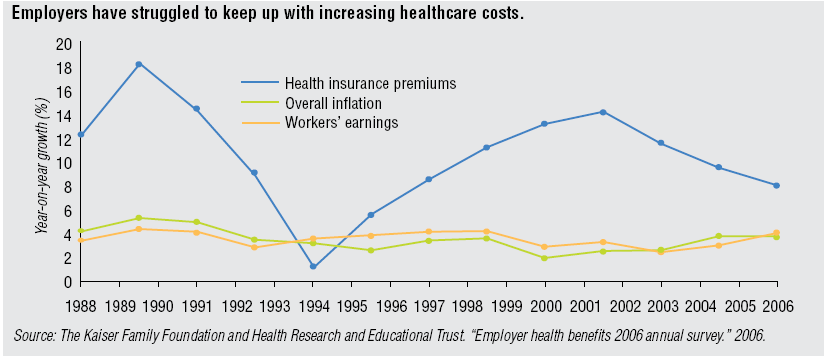

In the article, the authors (Barbara Martinez and Jacob Goldstein) predict that “over the next few years, the pharmaceutical business will hit a wall”. Their statistics on the movement to generics is even bigger than I remember. They say that roughly half of the manufacturer’s US sales are scheduled to lose patent between 2007 and 2012 (or more than 36 drugs representing $67B in annual US sales). (See charts from the article)

“The rise of generics wouldn’t matter so much if research labs were creating a stream of new hits. But that isn’t happening. During the five years from 2002 through 2006, the industry brought to market 43% fewer new chemical-based drugs than in the last five years of the 1990s, despite more than doubling research-and-development spending.”

“It has never been easy to take a drug from the lab, through animal testing and into human trials. The industry estimates only one out of every 5,000 to 10,000 candidates makes it to human trials. And many drugs that work beautifully in animals fail miserably in people.”

The article goes on to talk about regulation and the FDA and whether the lack of new products is their issue or some other issue such as the R&D organizational model. It also talks about the fact that not much has changed since the  1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition.

1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition.

Of course, targeting niche patient groups with biogenerics creates very expensive drugs such as the $200,000 a year that Genzyme charges for Cerezyme to treat Gaucher disease. [If you’re total market size is smaller but your costs to develop and bring a product to market stay the same, prices have to go up or no one will develop the products. It is a problem.]

Given the focus on generics in the market and by the payors along with the battle between brands and generics, I always find it interesting that some of the big companies own generic companies (e.g., Novartis owns Sandoz and Pfizer owns Greenstone). I guess if you can’t beat them…join them.

It will be interesting to see how the companies react. As I have talked about with friends for years, it is relatively easy to be a successful executive in a wildly growing company and industry. It is hard to be a successful executive and leader in a cost oriented industry that is contracting and where the competitive pressures are great. Can these guys make the transition?

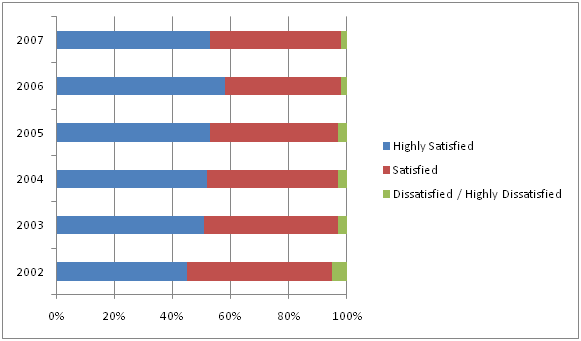

There is lots of data out there validating this as a focus. In

There is lots of data out there validating this as a focus. In  patients to try generic drugs. Earlier this year,

patients to try generic drugs. Earlier this year,  I had a chance to ride on a plane today with a man who sits on the board of a pharma company. He has worked in pharma for 30 years, and we had a good discussion. One of the things we talked about was the “arms race” in pharma to build up their number of detail representatives. Obviously this changed over the past few years especially with some of the limitations which have been placed on how pharma reps can incent physicians. We went on to talk about the challenge of physicians keeping up with all the drugs on the market and even understanding all the basic

I had a chance to ride on a plane today with a man who sits on the board of a pharma company. He has worked in pharma for 30 years, and we had a good discussion. One of the things we talked about was the “arms race” in pharma to build up their number of detail representatives. Obviously this changed over the past few years especially with some of the limitations which have been placed on how pharma reps can incent physicians. We went on to talk about the challenge of physicians keeping up with all the drugs on the market and even understanding all the basic  I have always found

I have always found  So, if you were responsible for your healthcare costs, would you rather have the Saturn model (i.e., lowest price is posted – no negotiation) or the jewelry model (i.e., retail price means nothing other than a point to negotiate from). This would be an interesting discussion as we get into more transparency about price / cost in healthcare services.

So, if you were responsible for your healthcare costs, would you rather have the Saturn model (i.e., lowest price is posted – no negotiation) or the jewelry model (i.e., retail price means nothing other than a point to negotiate from). This would be an interesting discussion as we get into more transparency about price / cost in healthcare services.