December 20, 2007

December 20, 2007

We used to talk a lot about stickiness of websites and eyeballs back in the late 1990s. The word still has some attraction and is a key point in the recent McKinsey interview with Chip Heath. Chip is a professor of Organizational Behavior at Stanford University’s Graduate School of Business.

“The key to effective communication: make it simple, make it concrete, and make it surprising.”

Although the article is primarily around what executives need to do to make their messaging and ideas stick with diverse audiences, it has a lot of relevance for healthcare.

“A sticky idea is one that people understand when they hear it, that they remember later on, and that changes something about the way they think or act.”

Think about all the things you want to tell your patients or members or employees (or vice-versa all the things you patients want your healthcare companies to tell you):

- There has been a change to your X (copay, formulary, network).

- You have an opportunity to save money by doing X.

- We are missing X data that will delay your coverage.

- We see that X happened and wanted to gather data on your experience or proactively address your question.

- Welcome to our plan. Have you registered on the website? Have you received your ID card?

- Please take this Health Risk Assessment.

- Your credit card has expired. Would you like to update it?

- Your order is delayed. If this is an emergency, please do X?

- We see you were on the website. Did you find what you needed?

- Do you need a copy of your X (formulary, provider directory)?

- You have not yet picked a Primary Care Physician. Would you like to do that now?

- Did you receive the information that we sent you?

- Are you following your physicians orders? Did you do X? Why or why not?

- Our records show us that you are due for a X. (Flu shot, screening)

- Are you using any over-the-counter products that we should have in our database to identify drug-drug interactions?

- Please remember to refill your medication?

- Are you having any side effects or complications associated with your recent medication or procedure?

- Have you enrolled yet in our disease management (or incentive) program? Would you like more information?

- Welcome to the plan.

- We know it is time for open enrollment. We hope you will renew with us. We are offering a local meeting to help you learn more about your benefits. Would you like to attend?

- X has changed with your drug, condition, etc. There is new information available at Y.

Getting back to the article…He offers several good examples of sticky messages which are primarily what I would call rallying calls for organizations. In healthcare, the key is to find these simple messages that compel people to act. So, bottom lining it, he gives six basic traits:

Getting back to the article…He offers several good examples of sticky messages which are primarily what I would call rallying calls for organizations. In healthcare, the key is to find these simple messages that compel people to act. So, bottom lining it, he gives six basic traits:

- Simplicity – short and deep

- Unexpectedness – uncommon sense messages generate interest and curiosity

- Concreteness – his example is don’t say “seize leadership in the space race” but say “get an American on the moon in this decade”

- Credibility – this should be so easy in healthcare if you leverage all the people and stories out there

- Emotions

- Stories

He has a few great stories such as:

- A Nordstrom’s person wrapping something bought at Macy’s just to make the customer happy. [And probably without point it out.]

- A FedEx driver who forgot the key to a box simply unbolting the box from the ground and throwing it in the truck so they weren’t late.

These things reinforce the message while becoming a type of urban legend that stay with people. They evoke emotion in a simple way.

One good example I have from Express Scripts was around trying to motivate people to change from one drug to another. When Zocor was going generic, we decided to launch a huge multi-modal campaign to drive down Lipitor marketshare and move people to Zocor so that when it went generic everyone would win. [Clients would save; patients would save; and we would make more money.] It worked. But, prior to the program, we worked with linguists and others to design and test a set of messages. The one that resided best was “we have a secret that can save you money”. People were intrigued and listened. They felt like they were being let in on something that was important. We ended up positioning it similar to a Consumer Reports Best Buy. It worked.

In

In

On 12/6/07, the

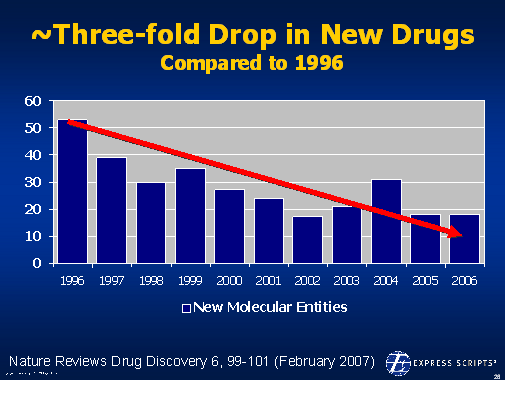

On 12/6/07, the  1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition.

1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition. There is lots of data out there validating this as a focus. In

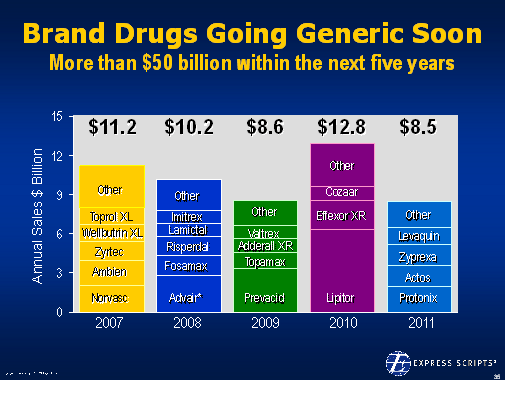

There is lots of data out there validating this as a focus. In  patients to try generic drugs. Earlier this year,

patients to try generic drugs. Earlier this year,