January 16, 2008

January 16, 2008

This has always been a topic that fascinates me. Learning from someone’s handwriting. So I liked seeing a cliff note summary of The Complete Idiot’s Guide to Handwriting Analysis by Sheila Lowe in Spirit Magazine. I am not sure I would be ready for this to be part of an employment process although I have taken personality tests such as Myers-Briggs (test yourself here) before.

Here are a couple of the items on handwriting:

- Balanced margins; clear spaces between words = ability to plan ahead

- All the letters connected in every word = logical thinker who enjoys debating to the point of nitpicking

- Abrupt breaks between letters = person who jumps to conclusions without the benefit of logic

- Large letters = loves the spotlight

- Small letters = finds more satisfaction in working then socializing

- Lots of rounded letters = outgoing person

- Straight lines and angles = aggressive person who pushes hard for what they want

- Lots of loops and close spaces between words = big imagination and need for social contact

- Few loops and wide spaces between words = intellectual loner

- Thin writing with illegible words = creative genius OR slippery character

- Hidden personality traits are seen in the lower loops of letters g, y, f, p, and z):

- Moderately wide loop = welcomes a variety of experiences

- Skinny loop = sticky to what they know

- Extremely wide loops = bragger who doesn’t follow through

- The upper loop slant measures emotional responsiveness:

- Extreme right slant = emotionally explosive

- Moderate right slant = warm and responsive

- Vertical = cool headed

- Left slant = friendly on the surface but hard to get to know

Now, I know you are dying to go look at your writing and see what it says about you.

He talks about the concentration of spending (based on Kaiser Permanente data):

He talks about the concentration of spending (based on Kaiser Permanente data): use that to compel the legislators to act but doesn’t it seem strange to have an end customer comment about the supply chain relationship of two entities. What am I talking about?

use that to compel the legislators to act but doesn’t it seem strange to have an end customer comment about the supply chain relationship of two entities. What am I talking about?

In

In

On 12/6/07, the

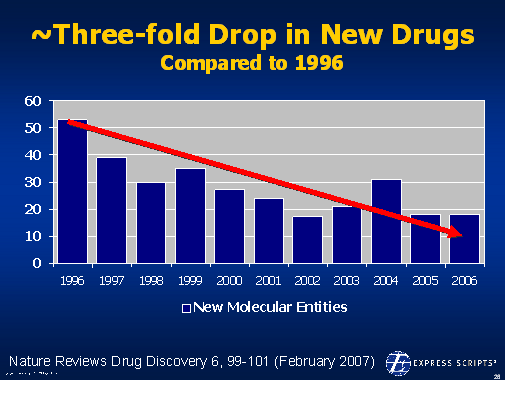

On 12/6/07, the  1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition.

1800s in terms of the framework for developing drugs. Obviously, this has been the driver for biotech where the drugs are made of proteins and there is no generic competition.

{kind=link}