On the surface, the “Holy Grail” of sophisticated wellness and incentives programs are based on outcomes. This means that the individual gets rewarded for achieving a goal. For example, you can structure your incentives different ways. You could have a reward for enrollment (i.e., I register for a program). You could have a reward for activity (i.e., I talk to a nurse or watch a video online). You could have a reward for an outcome (i.e., I lose 10 pounds).

But, those have different implications in terms of structure. [Note: I’m not a lawyer or an accountant so don’t take this as legal advice.] I think Andrea Davis at Employee Benefit News did a good job of touching on this in her article “No Good Deed“.

I did have a chance to implement a large outcomes-based rewards program for 1/1/14 where we had to address a lot of these changes from the ACA. One of the key terms that she hits on is this idea of “Reasonable Alternative Standards”. This basically means that if you implement an outcomes based incentive program that people have to be able to get the same incentive without achieving the outcome. This seems to defeat the purpose in my mind.

I always used to say that it was like having a guard dog with no teeth. We implemented a very interesting program with lots of expectations, but there was a huge gapping loop hole. Everyone could apply for a Reasonable Alternative Standard and achieve the same payout without really doing much. Of course, most people don’t realize this, but this is why I would argue that people that aren’t healthy or engaged with their health programs at work would rather have these outcomes based programs.

Do you ever hear someone talk about how great our healthcare system is because survival rates for a particular condition have gone up? Of course you have. Here’s one that says that cancer survival rates have doubled over the past 30 years.

This sounds great. We all get excited about this.

BUT…the key question that I have to ask is whether this is tied to better identification of cancer and early screening. If you screen more people and identify them earlier, you will have more survivors that live longer. That’s just a reality. For some people, the disease never will have progressed which is what leads us to this screening dilemma.

In the second article, they were looking for evidences of cancer in ancient societies to see what that might teach us about cancer. What I found most interesting was the comment about people believing that cancer was a modern disease attributed to our environment so that it didn’t exist long ago. I can see how all the articles about things leading to cancer could create that perception, but it seems like a big jump to me.

So, for those of you that are in healthcare, this is a great lesson about understanding the measures you use and how they drive actions. For those of you as consumers, this is a good reminder to understand the metrics that are thrown around and question them.

Ideally, we’d all get individualized or personalized healthcare, but we’re still years away from that happening. But, there are several basics about segmenting individuals which are relevant. One of them is that men and women are different in how they experience healthcare. Another one is that different plan designs drive different behaviors.

With those in mind, I found an article in the June 2014 Money magazine interesting. It pointed out that while both men and women reduce their use of the emergency room with high-deductible plans that it varies. As you can see from the table below, this is especially relevant for high-severity issues where men dramatically reduce their use of the ER which can lead to significant issues.

In the April 7, 2014 issue of Fortune magazine, they have an article by General George W. Casey Jr (retired) who talks about giving a presentation at UNC about this. From his article, he mentions a few key things:

It’s really difficult.

Leaders need to “see around corners”

You need a clear statement of what needs to be accomplished

I think it’s a great framework for start-ups and healthcare in general. We’re in a time of massive change in healthcare. It can lead to people being paralyzed by a lack of a clear future. Leaders need to help their team understand a future vision and give them a clear problem statement to solve. This will help drive action which is critical.

If you’ve never watched a video about Parkour running (aka free running), take a look at this video.

As a runner, I find this very interesting. On the flipside as someone who can’t do a cartwheel, is afraid of heights, and has passed 40, this seems like a great way for me to hurt myself.

But, I find it really interesting that a TV show based on an obstacle course in Japan has really shined a light on this. American Ninja Warrior is a very interesting show about athletes. It’s like the Voice for sports. They share the backstory and then have people compete on very difficult obstacles. You see NFL players, Olympic athletes, trainers, stuntmen, and people from all walks of live. I personally find it a great show to run on the treadmill with. I feel very motivated.

I thought I’d share as this looks like a great type of program for kids to get them into obstacle course running and making exercise fun. I know a lot of gyms around the country have started to offer these programs.

Let me start by saying…DON’T read this book if you enjoy having your physician up on a pedestal. It will change your perceptions and skepticism of the system.

DO read this book if you’re frustrated by our US health care system and wonder why we spend so much money without necessarily seeing differences in mortality and outcomes compared to other developed countries.

“Proponents of science as a foundation for health care have not come together to form a grassroots movement, and until this happens, all of us will have to live with a system built on pseudoscience, greed, myths, lies, fraud, and looking the other way. Patients need to learn that more care is not better care, that doctors are not necessarily right, and that some doctors are not even truthful.”

Otis W. Brawley, M.D., F.A.C.P., chief medical officer for the American Cancer Society, is responsible for promoting the goals of cancer prevention, early detection, and quality treatment through cancer research and education.

Dr. Brawley currently serves as professor of hematology, oncology, medicine and epidemiology at Emory University. From April of 2001 to November of 2007, he was medical director of the Georgia Cancer Center for Excellence at Grady Memorial Hospital in Atlanta, and deputy director for cancer control at Winship Cancer Institute at Emory University. He has also previously served as a member of the Society’s Prostate Cancer Committee, co-chaired the U.S. Surgeon General’s Task Force on Cancer Health Disparities, and filled a variety of capacities at the National Cancer Institute (NCI), most recently serving as assistant director.

Dr. Brawley is a member of the Centers for Disease Control and Prevention Advisory Committee on Breast Cancer in Young Women. He was formerly a member of the Centers for Disease Control and Prevention Breast and Cervical Cancer Early Detection and Control Advisory Committee. He served as a member of the Food and Drug Administration Oncologic Drug Advisory Committee and chaired the National Institute of Health Consensus Panel on the Treatment of Sickle Cell Disease.

Dr. Brawley is a graduate of University of Chicago, Pritzker School of Medicine. He completed his internship at University Hospitals of Cleveland, Case-Western Reserve University, his residency at University Hospital of Cleveland, and his fellowship at the National Cancer Institute.

I would put this book on my must read list for anyone working in healthcare. I have two other books there:

Here are some things I highlighted as I read the book:

People diagnosed with cancer who had no insurance or were insured through Medicaid were 1.6x more likely to die within 5 years than those with private insurance.

“No incident in American medicine should be dismissed as an aberration. Failure is the system.”

“Our medical system fails to provide care when care is needed and fails to stop expensive, often unnecessary, and frequently harmful interventions even in situations when science proves these interventions are wrongheaded.”

He introduces the concept of the “wallet biopsy” as a term to describe the difference in care we get once it’s determined what type of insurance we have.

While he points out and is clearly an advocate for health discrepancies and the issues of the un- and under-insured, he also points out that “wealth in America is no protection from getting lousy care”.

He hits on a point that I agree with in medicine and everywhere else which is teaching people to say “I don’t know”. He later says “If you truly respect the patients you treat, you will not obscure the line where your knowledge stops and your opinion begins.”

“In most cancers, the quality of the surgery is the most important factor in the ultimate outcome.”

He talks a lot about the motivation of physicians in determining treatment and how that can be misguided over time. While some of this can be explained away with Defensive Medicine, he points out that many other times this is simply the business of healthcare with people making money off these treatments. Or, as he also points out, sometimes it’s simply unwillingness to challenge the status quo of over-treating the patient. [This is something that I’ve heard other oncologists who provide second opinions point out.]

I learned about “gomers” which stands for get out of my emergency room which are patients who come to the emergency room just to interact with someone without any real symptoms. He also introduces several other terms apparently all derived from a book The House of God about an intership at Beth Israel Medical Center in the 70s.

He brings up an important issue that us as Americans and many physicians believe to be true which is that “death is a failure of medicine”. I’ve talked with several physicians about this. I believe it’s one of the things that contributes to the enormous amount of money we spend on people in their last 90-days of life.

He gives a great (but sad) story of the “moral hazard” scenario of a family trying to care for their parent in the last days of their life and all the “senseless acts of medical torture” that they put him through. This is one of his classic examples of where the physician knows better but is actually instructed to do harm.

He talks about one of the physicians he was assigned to work with during a rotation. I thought this summary of his rules was great:

“You don’t deviate from the science. You don’t make it up as you are going along. You have to have a reason to give the drugs you are giving. You have to be able to quote literature that supports what you are doing. You have to tell patients the truth.”

At one point, he says that he confirms a truth he learned as a kid which is scary – “Doctors try out things just to see whether they will work.”

He gives a brief nod to companies using business rules to safeguard patients through technology that requires physicians to document what they are doing and comparing those to guidelines.

He spends a lot of time on prevention and survivorship in terms of how people justify some of those numbers. It’s worthy of an entire post, but the key point is that early diagnosis by itself simply increases the years of survivorship. It doesn’t actually mean we did anything better. He also points out that due to all the treatments we give patients some of them die of other issues rather than cancer that “improves” the cancer death statistics.

And, for all of my pharmacy friends, he doesn’t miss the opportunity to tell the Nexium story or to talk about Vioxx and what happened in both of those cases.

His stories are amazingly similar to some of the physicians that I worked with for the past two years. He talks about the overuse of radiologic imaging. He talks about the da Vinci robot.

He gives some unique insights into the politics of support groups and government funding which I’d never understood before.

A great quote he uses from Willet Whitmore when talking about PSA testing and prostate cancer was:

“When cure is possible, is it necessary, and when cure is necessary, is it possible?”

I also liked a quote he gave from another urologist which said:

“There is the kind of prostate cancer that can be cured, but does not need to be cured; there is the kind of prostate cancer that needs to be cured and cannot be. We all hope there is a kind of prostate cancer that needs to be cured and can be cured.”

This leads up to his point that research shows that 1.3M American men were needlessly treated for localized prostate cancer from 1986-2005. Wow!

He was very positive on the US Preventative Services Task Force (USPSTF) which I was glad to hear since that’s the group that several of my physician friends have used before for setting guidelines.

Hopefully, you get the point. It’s a quick read with a good mix of studies, patient stories, and the history of cancer with a focus on both historical and current issues that face us in this time of transformation in health care.

Here’s a few more articles about Dr. Brawley and his book:

As a random point of interest, Dr. Brawley uses several references to teachers and his Jesuit education at The University of Detroit Jesuit High School and Academy in Detroit which is where I also went to school and had some of the same teachers. Our school was featured a few years ago as the last Catholic college prep school still in the city.

After Aetna, Cigna, and Wellpoint all moved into different PBM relationships with CVS Caremark, CatamaranRx, and Express Scripts, it certainly marked the end of much of the debate on whether a captive PBM (i.e., owned and integrated with the managed care company) could compete with the standalone PBMs. There are really only a few big integrated models left including Humana, OptumRx (as part of UHG) and Kaiser with Prime Therapeutics having a mixed model of ownership by a group of Blues plans but run as a standalone entity. Regardless of where the latest Humana rumors take them, it made me think about what the market has become with these new relationships.

Scale matters. All of these relationships and discussions show that there are clear efficiencies in the marketplace.

Drug procurement (i.e., negotiating with the manufacturers (brand and generic) and the wholesalers)

Pharmacy networks (i.e., getting the lowest price for reimbursement with the retail pharmacies)

Rebating (i.e., negotiating with the brand and specialty drug manufacturers for rebates)

Outcomes matter. If scale was all that mattered, there be no room for others in the marketplace. But, we continue to see people look at this market and try to make money. That means that “outcomes” matter in different ways:

Clinical outcomes (i.e., does the PBM have clinical programs or intervention strategies that improve adherence and/or can demonstrate an ability to lower re-admissions or impact other healthcare costs?)

Financial outcomes (i.e., does the PBM have innovative programs around utilization management (step therapy, prior authorization, quantity level limit) or other programs like academic detailing that impact costs?)

Consumer experience (i.e., does the PBM’s mail order process or customer service process or member engagement (digital, call center, etc) drive a better experience which improves overall satisfaction and overall engagement…which drives outcomes?)

Physician experience (i.e., does the PBM engage the physician community especially in specialty areas like oncology to work collaboratively to drive different outcomes?)

Data (i.e., does the PBM use data in scientifically valid but creative ways to create new actionable insights into the population and the behavior to find new ways of saving money and improving outcomes?)

While I’ve been beating the drug of the risks of commoditization to the market for years, I’m going to make a nuanced shift in my discussions to say that there is still a risk of commoditization and driving down to the lowest cost, but we may be quickly approaching that point. What I’m realizing is that there can be a two tier strategy where you commoditize certain areas of the business and let the other areas be differentiated. And, that this can be a survival tactic where you either outsource the core transactional processes to one of these low cost providers or figure out how to be one of them while creating strategic differentiation in other areas.

I was reading my AIS Health Business Daily e-mail this morning. Today’s quote of the day is below. It made me wonder. Think about any healthcare organization. We have a long way to go to get here.

“The other part … of a great customer experience is to have a seamless interaction. The last thing we want to hear is ‘oh, I can’t help you, that’s his department’ or ‘I can’t help you, it’s his operating division’ or ‘I can’t help you because Sally helped you with that; I’m Sue.’ That’s not going to work. A great customer experience is when it is seamless. Customers look at us as a brand, as Nordstrom, as one. However we’re organized with our people, how we operate, customers don’t care about that. They care about what you stand for and the seamless customer experience.”

— Mike Koppel, Executive Vice President and CFO at Nordstrom Inc., speaking recently at America’s Health Insurance Plans’ Institute 2014 in Seattle.

It was good because I actually heard things that I’d never heard discussed around specialty pharmacy before. And, as he pointed out, specialty will represent 50% of the pharmacy spend and about $235B in total spend by 2018. This is where everyone is focused and the opportunity for differentiation exists.

He talked about how to get to zero trend in specialty.

He talked about the consumer experience in specialty.

He talked about care coordination and its value in specialty.

He talked about the need for a beyond the pill approach by the specialty pharmacy.

So, what does all this mean? Let me share some highlights:

Specialty pricing is starting higher based on government pricing constraints. You can’t raise price. It’s easier to start high, discount, and/or come down over time.

3.6% of patients drive 25% of costs (not a surprise)…but 43% of their total costs are not from the specialty condition but from their co-morbidities. (Why treating the patient not the condition is critical.)

Site of care (which is the hot buzz today) can save you 17% or more.

Developing an exclusion formulary is important to counteract copay cards and help reduce costs.

They are moving from 12-month contracting with pharma to 2-3 month contracts to really keep on top of market conditions.

Coordinated care can drive lower costs in terms of readmissions and other total medical costs.

You can use generics to replace biologics. For example, he showed switching out an HIV biologic costing almost $3,000 / month with 3 generics costing $101 per month. (I’ve never heard anyone else talk about this.)

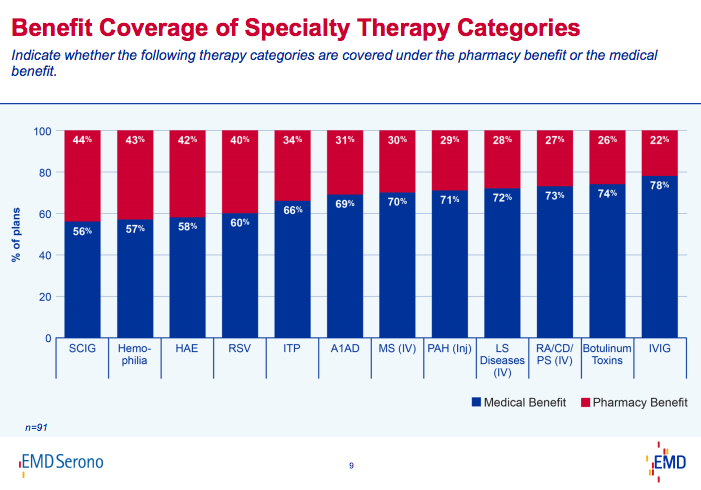

He also reinforced the fact that today’s specialty benefits are not coordinated across medical and pharmacy. For example, he used the RA example where there are 9 drugs with 4 of them commonly used under the medical benefit and 5 under the pharmacy benefit.

But, the most important thing was their strategy to get clients to ZERO TREND for specialty pharmacy. (It reminded me of the program I developed at Express Scripts where we actually guaranteed a 3-year zero trend…if you followed our very aggressive recommendations.) He outlined the following:

1.5% savings from their formulary

0.5% savings from an exclusive specialty network

1.9% savings from an aggressive generic policy

1.0% savings from innovative pricing

3.6% savings from optimizing site of care

2.5% savings from medical claims editing and repricing

6.0% savings from enhanced prior authorization

He also went on to talk about the consumer experience. I think a lot of specialty pharmacies are thinking about the same things, but there were several things he shared that were new to me. It was exciting.

As I’ve said before, as specialty pharmacies really start to think about the patient and focus on the experience over time, we will start to see more coordination with pharma about going beyond the pill and driving lower total costs.

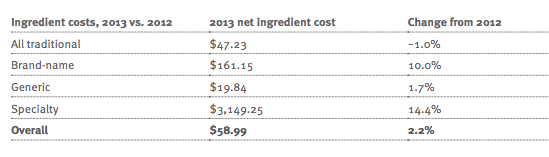

The Prime Therapeutics Drug Trend Report was released yesterday. Interestingly, they start out the report by making the point that what really should matter is net ingredient cost not trend. I’ve made the point before that trend isn’t a great number to focus on for many reasons. And, if you’re comparing trend numbers (which we all do), then you need to understand different methodologies. I think Adam Fein does a good job of summarizing that in his post. (BTW – This is a tough discussion to have especially when you’re getting spreadsheeted by consultants as part of an RFP.)

As comparisons, you can see my reviews of the other drug trend reports here:

Their report was short and to the point. Here’s some of the key data points:

25M members

80.6% generic fill rate

12.7 Rxs PMPY

Overall drug trend = 3.3%

Specialty drug trend = 19.5%

Net ingredient cost trend = 2.2%

The net ingredient cost per Rx = $58.99 (this is net of rebates and takes into account acquisition costs and network discounts)

They state that this beats the competition by $6.00 per Rx

Of course, anything anyone really cares about these days is specialty. Specialty represents only 0.4% of the scripts they fill but 20.5% of the spend for a commercial account. (They point out that this is much less as a percentage of scripts than other PBMs which have closer to 1% of their scripts classified as specialty…which could influence trend numbers.) The chart below shows how some of the things we all did around traditional drugs apply to specialty drugs.

For some people running mail order pharmacies, this analysis is no big surprise. They’re running off to their boss to show them that it’s not just their mail order facility, but it’s an industry issue. To others, they’re left scratching their head trying to figure out why this is. If mail order is where all the money is, what does this mean to them? (The historical PBM model put most profit in generics filled at mail order.)

At the end of the day, I simplify the mail order issue down to four major challenges:

Savings are disappearing. Savings were primarily on brand drugs filled for 90-days. When you fill a generic at mail and your getting 15-30 days supply for “free” (i.e., no copay), that’s great, but the copay savings is $4-10 every 90-days. With generic utilization in or around 80%, this is a real issue.

Transparency, coupons, and cash pay. With apps like GoodRx, it’s easy for consumers to find the lowest cost option for them to fill a prescription. That might be in a discount program. It might be to pay cash. It might be with a coupon. And, it might be mail order. They now can figure it out and optimize their spend easier. Mail isn’t the only option.

High expectations. As a society, we continue to be more and more of a society that wants an instant response. Sending prescriptions off to a black box with a multiple day turnaround and difficulty tracking the prescription doesn’t meet our modern expectations. (A connected model of electronic prescribing may one day change this.)

Cash flow. As I always point out to people, we (those working in the industry) don’t represent the average American. While it seems so logical to pay for a 90-day script in order to save money, that means you have to have the cash to pay for 3 months upfront. Not everyone can do that especially when they have multiple prescriptions…And, no mail order pharmacy that I know of wants to be in the credit business.

Will mail order disappear? Of course not, but PBMs need to continue to either find ways to improve the consumer experience and make it better or they need to recognize the issues that exist and continue to diversify. And, with more 90-day prescriptions at retail for the same copay (i.e., CVS Caremark), this will continue to shift expectations.

I think this is really interesting. Cleveland Clinic has opened a Chinese herbal-therapy ward. In the US, we’re very much a medicated society. There’s a pill for almost every ailment you have and some you didn’t even know you had. Even admitting that Western medicine might not have all the answers is a big step forward especially for such as prestigious hospital such as Cleveland Clinic.

So, what are they doing? According to what I’ve read, they see patients with chronic pain, fatigue, poor digestion, infertility, and sleep disorders. The clinic is run by a certified herbalist under the supervision of several classically trained physicians. Access to the clinic is only on a referral basis, and according to Ohio law, the physician has to continue to oversee the patient’s treatment for a year after their referral.

The clinic is a single room with bright pillows, a tapestry, candles, and a cot.

Compared to China, the herbal formulas here are all encapsulated versus sent home with them to brew.

Of course, one of the worries is drug-herb interactions which requires them to coordinate care using an EMR and have people that have the right training and work with a clinic that can provide them with the right herbs and still meet their safety standards.

A consultation costs $100 which is typically not covered by insurance. Additionally, follow-ups are $60 and a one-month supply of herbs will cost $100 (on average).

Back in March 2014 (yes I’m behind), Fast Company put out a report on the World’s Most Innovative Companies. I thought the list of 12 trends or lessons from their research was worth sharing.

Exceptional is the Expected…Google is the case study here, but they make a point that for most companies, the best businesses focus on less not more.

Innovation is Episodic…Innovation ebbs and flows so people don’t stay on the list every year. This is also known as regression to the mean or the Sports Illustrated curse (of being on the cover).

Making Money Matters…This is very true for mHealth. I’ve seen so many really cool ideas, but if they’re not self-sustaining, that’s a problem.

Sustainability Has Found A New Gear…”Green” is no longer a gimmick. Companies are innovating and using alternative fuels and recycling as part of that.

Unlocking Global Talent Unlocks Possibility…I can’t believe companies still don’t get this. To innovate, you need diversity and a culture which allows those different opinions and perspectives to hash it solutions. (Just look at the graphic at the bottom of this post for Silicon Valley which makes that point.)

Passion is Underrated…While crowdsourcing sounds like old news to many industries. I think there’s still a huge patient empowerment push that will happen in healthcare. (Just look at this article in the WSJ.)

Conflict Isn’t Required…This is the perfect Blue Ocean example. You don’t always have to try to change the establishment but sometimes you have to figure out a whole new way.

Happy Customers Make You Happy…Not much to say here. Healthcare is about to learn this lesson with exchanges, but we have a long way to go.

Software Beats Hardware…YES! A great computer with a horrible data entry process which messes up the physician workflow and consumer experience is bad. We need outside-in design to develop user-friendly software that takes into account workflow and regulation but improves the overall experience and outcomes.

“Made In China” Is A Compliment…I’d expand this point to say that while we’ve outsourced for years for cost that’s building up knowledge and a middle class abroad. As their expectations and experience rise, we’re going to see more innovation and quality from abroad.

Dreaming Big Isn’t Folly; It’s Required…Eliminating cancer. Changing payment paradigms in healthcare. Getting patients to take action. Changing food at schools. We have to have some BHAGs in healthcare and make them happen. (Perhaps some of the HealthPeople 2020 initiatives will get us thinking.)

Above: Tech Immigrants: A Map of Silicon Valley’s Imported Talent (from VentureBeat article)

Curing Camden is a quick read on how different groups collaborated to change the healthcare cost curve in Camden, NJ. Here’s the official language from the Amazon site, but after reading it, I thought I’d highlight a few things that caught my attention.

As the federal health reform debate played out in the national media spotlight, author Christina Hernandez Sherwood was reporting on the American medical system from the street level. From 2010 to 2012, she wrote a half-dozen stories for thePhiladelphia Inquirer that focused on an innovative healthcare nonprofit: the Camden Coalition of Healthcare Providers. These stories centered on the nonprofit’s role in combating falls, violence, diabetes, and other issues in Camden, New Jersey, a city known nationally as one of the country’s poorest and most violent, but that is now making a name for itself as an innovation leader in the public health sector.

In Curing Camden, all of Sherwood’s articles have been collected into a single book, including the unpublished final installment profiling the nonprofit’s founder. This book takes readers from the living rooms of Camden residents to the halls of the New Jersey State House in Trenton and beyond. Sherwood highlights how Camden could be the first US city to bend the cost curve by lowering healthcare costs while improving care. The ideas revealed in this book could be translated into practice across the country, and Camden could become a national model of 21st century medicine and public health.

The book goes through several core chapters. The first one is on creating a citywide health record by working with the 3 primary health systems in the city. The core part of the success here is that they used the framework of opt-out not opt-in which would drive more participation at the consumer level. This behavioral economics framework called “active choice” has been used by several companies that I’ve worked with in the healthcare space to shift behavior patterns. This obviously has the opportunity to reduce duplicate testing and improve care coordination.

The second chapter is about create an ACO for Camden with a 3-year Medicare demonstration project. It’s an interesting discussion about how Dr. Jeffrey Brenner began using data to learn things about the Camden population. For example he found out that most of the population will vista a hospital at least once in a 2-year period (which is 2x the national rate). He also found that most of the top reasons for going to the emergency room were all primary care issues. He makes a great point in the book that while people think that complicated patients simply like going to emergency rooms the reality is that they don’t have better choices.

The third chapter was about protecting against the risk of falling. From 2002-2009, Camden residents made more than 17,000 trips to the hospital (the number one cause of hospital visits in Camden). This isn’t a localized issue either. Falls affect 1 in 3 seniors every year and drive $19B in costs according to the CDC. In the book, they make an interesting point about the “vicious cycle” of falling which leads to less activity which leads to weaker patients increasing the likelihood of another fall.

The fourth and fifth chapters are about diabetes. In Camden, almost 13% of adults have diabetes. These patients can be high utilizers which is something they talk about along with their focus on the 13% of patients that drive more than 80% of the costs in Camden with one patient having over $5M in charges over 5 years. Of course, people in dangerous communities are at higher risk of obesity due to lack of access to food and safe places to exercise which contributes to the diabetes issues.

The sixth chapter is about violence and helping victims. Camden’s 77,000 residents experience more than 13 aggravated assaults per 1,000 residents (which is 5x the national rate). This lead to 9,361 trips to the hospital from 2002-2009.

It’s an interesting read. They had a lot of grant money, but at the end of the day, it was about several things:

Coordination and collaboration across the different systems

Localized care – being in the apartment building with a clinic or going into people’s homes

Using data to target the areas where they could make a difference

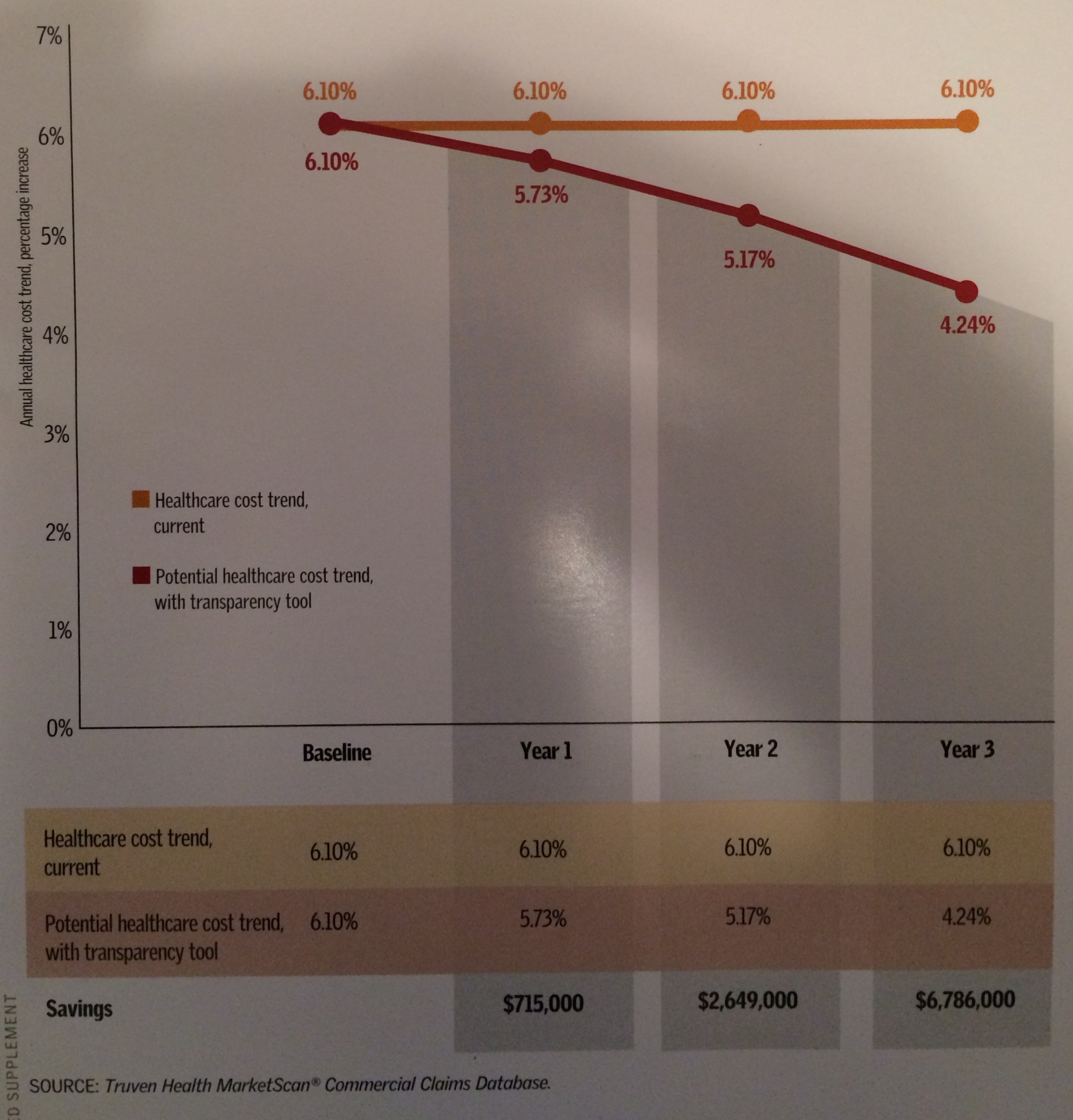

At the front of the HealthLeaders Magazine, they have a FactFile every month with data from Truven Health. The one from March 2014 focused on price variation and transparency. I thought I’d share a few of the charts.

This first chart shows their projections about the impact of a price transparency tool on cost savings over three years. (BTW – If you’re looking for information on price transparency tools, I would go to Jane Sarasohn-Kahn‘s blog HealthPopuli and look at her posts on transparency – Part I, Part II, Part III, Part IV, and Part V). Their projection was $6,786,000 in year 3 for an employer with 20,000 employees (or about 46,000 total covered lives if you assume a ratio of 2.3).

The other topic in the FactFile is about price variation and potential savings. They looked at three procedures and the variation in pricing for them. They then estimated the savings from those three procedures for an Chicago based employers.

As you can see, the variation is dramatic. What this will eventually lead to is called “reference-based pricing” where payers will agree to pay a fixed amount (or reference price) for a procedure and consumers will have to use transparency tools to figure out which providers will meet that price or pay out of pocket to go elsewhere. The hope is that this will drive down prices, make consumers aware of differences, and finally help people understand that price and quality are NOT correlated in healthcare.

Here’s a few articles to read on price transparency:

For those that are part of the Quantified Self movement, this is just a natural extension. You can now measure your different sports.

Swingbyte – a sensor that clips to your golf club to monitor speed, acceleration, arc, and other stats.

94Fifty Smart Sensor Basketball – a sensor embedded in a basketball to track shot speed, arc, and backspin along with dribble speed and force.

FWD Powershot – a sensor that fits into the handle end of a hockey stick and measures speed, angle, and acceleration.

Zepp Baseball Sensor – a sensor stuck to the knob of a baseball bat that tracks the speed and plane of the swing and the angle of impact.

There’s also the Babolat Play which is a smart tennis racket.

On the one hand, this stuff is fascinating and amazingly cool. On the other hand, who even knew that dribble force was something for me to be coached on. It will be interesting to see how athletes and coaches adopt these technologies and how they help improve sports over time. Will they increase the stress for the average athlete who was never going to be great and was just playing for fun? Will they improve everyone and help players and coaches really focus where they can make a difference?

This was just one of the really great data points I got from the Medication Adherence Clinical Reference page from the American College of Preventative Medicine. It’s worth a read.

But, let me highlight a few other points:

Non-adherence is thought to account for 30-50% of treatment failures.

Trust and communication are critical factors in adherence.

I think this is important because a lot of the industry solutions focus on the pharmacy and the consumer. They don’t (IMHO) go back to the initial discussion with the provider. How are we helping to enable those conversations to last longer than 99 seconds in the average encounter in which time they have to explain the medication, the side effects, and help the patient feel like the medication is going to make a difference? (Of course, this always make me think of my favorite placebo effect video.)

Additionally, this chart from the Adult Meducation publication was a great list of factors reported to impact adherence. (Sources: Miller et al., 1997; Nichols-English and Poirier, 2000; Vermiere et al., 2001; World Health Organization, 2003; Krueger et al., 2005; Osterberg and Blaschke, 2005)

They also share this chart (which I’ve seen a version of many times):

[Source: National Association of Chain Drug Stores, Pharmacies: Improving Health, Reducing Costs, July 2010. Based on IMS Health data]

There was an interesting story which came out of Michigan this past week from Christy Duffy about how her physician’s office was requiring all minors between the age of 12-17 to have a 5 minute private conversation with them (according to the law). Of course, it appears that they made a mistake per her later post, but I think it serves to make several interesting points.

1. Don’t always assume that someone’s interpretation of the law is right if it doesn’t make sense. Sometimes, you have to apply common sense and push back or ask questions.

2. There is a gray area between protecting the rights of our kids and protecting our rights. While the intent of allowing our kids to have honest and open conversations is appropriate, there needs to be some involvement of the parents.

It’s an interesting topic for discussion. Should our teenagers have access to providers on their own? Yes. If a teenager has a health issue, I think we’d all prefer that they talk to a professional rather than Dr. Google or their friends to find the answer.

Should a provider be able to force a private conversation with a minor? Yes…if they have a legitimate concern about abuse, but I don’t see any other reason.

Should a teenager who’s covered by my insurance and lives in my house be able to block me from having access to their medical records? Yes. This is the law, but should providers be having private conversations to offer them this option? I don’t think so. I would like them to have those discussions with me and my child to say that here are their options.

Should a teenager have a private conversation with their provider about STDs, HIV, and birth control? Yes, BUT I’d like to have the conversation at the right age with me in the room initially and then offer the private option. I don’t think forcing that conversation on a 12-year old would make sense in a private setting.

Ultimately, this comes down to the issue of access to the medical records online. What I heard was that this would also require the provider to get a cell phone and e-mail address for my kids. Obviously, if they’re doing something confidentially with the doctor, that’s one thing, but as a matter of record, I disagree. (I don’t even give out my kid’s Social Security numbers.) I don’t want my kids to start getting e-mails, phone calls, and letters sent directly to them as early as 12-years old. And, yes…I do try to shelter them a little. We talk about all the issues, but in a way that my wife and I want them to learn, not according to some formula driven approach that’s mandated. But, ultimately, I don’t think a 12-year old is mature enough to make all their own health decisions or to feel like they should.

Obviously, some part of this falls on the parent regardless to create an environment of open dialogue with their kids. The kids have to feel comfortable talking with their parents which is important for health and many other challenges that our kids have to deal with. And, unfortunately there’s always bad people in any profession so while sexual abuse by a physician or nurse is rare it’s not unheard of. Ideally, I think you should have the choice of when to encourage a private conversation and never have it mandated (unless of course the provider suspects abuse). Unfortunately, with a report of abuse being made every 10 seconds, we have a huge problem in our country.

I was reading an article the other day about devices like FitBit and their use within corporate wellness programs. One of the questions it was asking was why use them when people abandon them after a while. I found this great chart from Endeavour Partners in their whitepaper which looks a lot like an adherence curve. They say that 1/3 of people abandon their devices within 6 months which makes it a hard investment for anyone.

It’s the same question you might ask around mobile apps. While this chart shows that Americans install almost 33 apps, the questions is how long they use them.

According to Flurry, most apps peak within 3 months, and they show that health and fitness app retention is only 30% after 90-days. Again, that doesn’t make you want to invest a lot of money in a mobile app. But, there are lots of reports out there telling us that people want to use mobile to communicate with their providers, track calories, and do lots of other health related tasks. (see RuderFinn report, see IMS report, see Pew report)

So, what gives? Do we have unreasonable expectations? I would say yes.

We live in a ADD culture where people are constantly multi-tasking. People want things that evolve and constantly change. It’s the same reason we don’t want the same experience every single day. It’s the reason that you’ve seen people from gaming coming into healthcare. They understand how to keep people engaged over time.

Whether you want to picture it as a customer journey or different phases, the reality is that messaging needs to evolve with the consumer. If you got the same letter every month, at some point, you don’t even pay any attention to it. At some point, you wouldn’t even open it.

When I worked in healthcare communications, it was the same challenge from a strategy perspective. How would we coordinate communications across channels? What would the first message say versus the fifth message? How do you avoid message or channel fatigue?

It’s the same thing in the digital or device world. So, I ask the question…do we have unreasonable expectations about these tools by thinking that we can put them out there and sustain use of them? I think so. We need an evolving, constantly changing strategy about content, community, functionality, etc. to keep engagement sustained.

First CVS Caremark began offering mail order (90-day Rxs at lower cost) at retail stores (aka Maintenance Choice), and now with Specialty Connect, they are doing the same thing in specialty pharmacy.

Specialty Connect was a pilot program that won the PBMI Innovation Award this year. What it does is to allow consumers the choice of getting their specialty medications at either the CVS Caremark specialty pharmacy or picking them up at a local store. This is a change since: (1) many pharmacies don’t typically stock specialty medications; (2) many PBMs require use of a specialty pharmacy (i.e., mail); and (3) specialty medications typically require some addition handling and counseling which may be difficult to do at a local store level.

But, this is a very consumer friendly solution, and it has had some positive initial success. Here’s a quote and some data from their press release: (some additional data in the original PBMI document)

“Specialty Connect helps specialty patients with these critical therapies by helping to eliminate common challenges they had often faced and by offering them flexibility and choice,” said Alan Lotvin, M.D., Executive Vice President of Specialty Pharmacy for CVS Caremark. “The program makes it easier and more convenient for patients to submit and receive their specialty prescriptions either through CVS/pharmacy or by mail. What’s more, it increases medication adherence, improves outcomes and lowers overall health care costs for specialty patients and payors.”

Specialty Connect has demonstrated high levels of patient satisfaction as well as improved adherence for specialty pharmacy patients. In fact, pilot program results demonstrated a 13 percentage point increase (from 66 to 79 percent) in patients who were optimally adherent to their medication. Early program results also show that the program is improving upon the patient experience and reducing traditional barriers to getting started on medication, with 97 percent of patients successfully starting on therapy after only their first interaction at a CVS/pharmacy store. In addition, more than half of patients, many of whom were existing mail service pharmacy customers, chose to pick up their specialty medications at CVS/pharmacy.

Hopefully, this and many of the other CVS Caremark successes will make people wonder why they ever wanted to break the company up into different business units. As I’ve said for years on the blog, in the press, and to many Wall Street analysts, the integration of the business units can offer huge value once the synergies are realized and the consumer experience is integrated.

The other interesting things that I thought about when reading about Specialty Connect were:

It’s great to offer a centralized call center to support specialty but will that be enough at the local store level? Will patients want some type of higher touch local presence? Can that be achieved through a telemedicine or kiosk type solution?

I remember about 5 years ago when most specialty people thought they had to treat patients with specialty diseases differently. I kept trying to argue that they are just like other consumers. You should think about the experience across channels and at the patient not just condition level. This seems to signal a movement towards this. They are using SMS (text messages) and other channels to communicate with them which was a foreign concept a few years ago.

One of the things it highlighted is the incredible use of Wikipedia for healthcare information. People are typically going to Google and looking for a disease. Based on Wikipedia’s page rankings, this often leads them there.

Now, what makes this more interesting is the article in the BBC News which says that 90% of wikipedia articles on health contain errors.

Of course, the trick in reading the article closely is that it says they found that “90% of the entries made statements that contradicted latest medical research”. What’s the difference? Well, we know that it takes years for evidence-based medicine to become adopted within healthcare. So, how long does it take the latest medical research to get updated on all the sites? What I would love to see is a comparison of Wikipedia to WebMD, Ebix, and Healthwise. That would be telling.

When I saw this article and image in JAMA, I was really excited. It’s a good collection of structured and unstructured data sources. It reminded me of Dr. Harry Greenspun’s tweet from earlier today which points out why this new thinking is important.

People share more accurate #health & #lifestyle info through social media than with docs, what does that mean for…

— Harry Greenspun, MD (@harrygreenspun) May 27, 2014

But, it also made me think about this image and what was missing. The chart shows all the obvious data sources:

Pharmacy

Medical

Lab

Demographic

EMR / PHR

It even points out some of the newer sources of data:

Facebook

Twitter

Online communities

Genetics

But, I think they missed several that I think are important and relevant:

These things seem more relevant to me than fitness club memberships (which doesn’t actually mean you go to the fitness club) or ancestry.com data which isn’t very personalized (to the best of my knowledge).

In some cases, just simply understanding how consumers are using the healthcare system might be revealing and provide a perspective on their health literacy.

Do they call the Nurseline?

Do they go to the ER?

Do they have a PCP?

Do they use the EAP?

We’d like to think this was all coordinated (and sometimes scared into believing that it is), but the reality is that these data silos exist with limited ability to track a patient longitudinally and be sure that the patient is the same across data sources without a common, unique identifier.

The 5/26/14 edition of Forbes has a great article on Novartis called “Will This Man Cure Cancer?”. It’s an interesting article and Novartis has really ramped up their focus on Oncology with their purchase of Glaxo’s Cancer drugs. And, they recently got FDA approval for a lung cancer drug of theirs.

The article talks about Joseph Jimenez’s leadership at Novartis and highlights several interesting things:

A focus on speed to stop having to turn patients away from a possible cure.

Cancer drugs already represent $11.2B of Novartis’ $58B in sales.

Novartis has a 33% stake in Roche which has $31B in oncology sales.

Gleevec was it’s big breakthrough oncology drug that Jimenez’s predecessor believed in and has been so successful that it’s a $4.6B drug where they’ve been able to quadruple the price.

It talks about transforming the campus working with architects like Frank Gehry and moving research to Cambridge, MA.

There is some discussion on a new therapy that they’re working on based on some initial trials which uses CARTs (Chimeric Antigen Receptor T-Cells) to attach cancer. At the same time, Juno Therapeutics is on the same trail and raised $175M in their first round to research it.

I really liked one quote from Jimenez in the article that seems to imply a focus on the end goal not necessarily whether they win.

“You look at a company like Celgene, and you know they’re going to figure it out. And they should figure it out. It will be good for patients. We want to beat the competition, but we’re really using the competition to trigger us to get to the patient.”

He goes on to talk about the issue of pricing especially around oncology drugs (but also applicable to specialty drugs in general). He calls it “a new brutal world” because costs will go up with the aging population and new medicines which will cause more backlash against price. He talks about looking at how to be innovative about pricing which could be interesting.

“Payers are primarily dissatisfied with their specialty pharmacy’s ability to document the interventions they say they are performing. As pharmacies compete on price and service, they will need to be able to efficiently document the services they perform in order to differentiate themselves in the marketplace.”

The point is that complex conditions like oncology are a lot more than simply filling the drug. To be truly patient-centric, you need to be able to answer all these questions:

Were they diagnosed correctly?

Were they staged correctly?

Did the provider follow evidence-based care? From NCCN? From a particular pathway?

Did they get all the genetic tests done?

Did they get too many tests?

Are they prescribed the right drug? Will that drug limit any future options for care?

Is the drug covered on formulary? If not, are there other ways to reduce the out-of-pocket costs to the member?

Is it a limited distribution drug?

Do they understand the side effects of the drug and/or treatment?

What does the patient want? What do they know?

Do they have a caregiver? How are they involved?

Are they getting the drug at the right site-of-care?

Are they working with a case manager? How is their care being coordinated?

What’s the survival rate?

Are there implications for ongoing care as a cancer survivor? How will they be coordinated?

If they need palliative care, what are their wishes? Does the family, patient, and provider all agree?

Cancer is a great example of where everything comes together from a care coordination, testing, diagnosis, delivery, and pharmacy perspective. At the same time, we know that patients still see multiple doctors who don’t coordinate their care. We know they get mis-diagnosed. We know that don’t stay adherent with their medications. We know they don’t always articulate their wishes. And, we know the amount of care spent in the last months of life is disproportionate (IMHO) to the minor life extension which they get (often in less than optimal conditions).

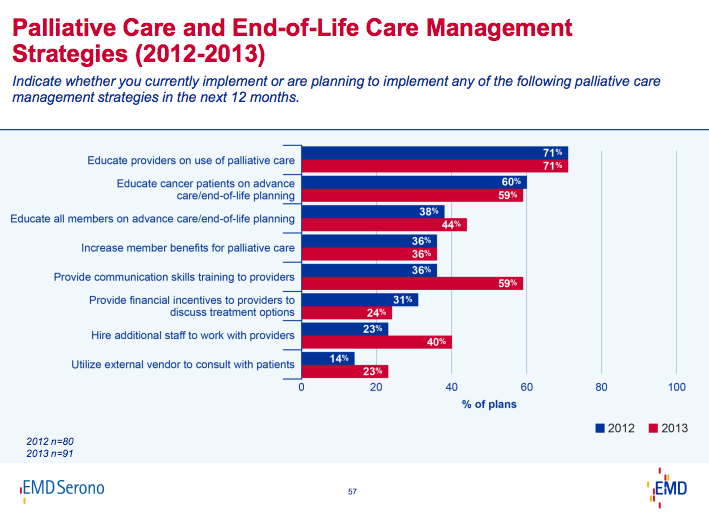

Here’s a good summary of some key data from the EMD Serono report:

It’s not a healthcare focused report so you have to gleam a few things from his summaries although you can buy the report to see the details by company. Without doing that, I thought I’d point out a few things from his charts.

1. Humana was the most improved (of all companies) in terms of customer service. Great job. Coventry (which was bought by Aetna) had the biggest drop (of all companies) in terms of customer service. [Perhaps not a big surprise as integrations can always be tough.]

2. As it has in past years, healthcare continues to be at low end of the spectrum in terms of customer service. While you can divide up the market into pharmacies, physicians, hospitals, PBMs, and insurance companies (with many other players out there), one of the biggest groups which is covered in the survey is health insurance companies. They fall below airlines and way below other types of insurance companies – i.e., auto / home.

“Hubbub is a technology-driven online playground and mobile wellness solution that uses social circles and gamification to motivate and engage people in healthy behaviors.”

Several people have suggested I take a look at what Hubbub Health is doing so I did. At first glance, there were several things that caught my attention (beyond the interesting teaser description of the company):

Lots of unconventional language in how they talk (reminds me of the Wellpoint Tonik Healthcare business from years ago)

A direct to consumer model where you can download the app and use their tool AND a $3 PMPM (per member per month) model for employers which includes additional services like health coaching (most people aren’t in both markets)

Of course the question is whether this is just another one of many mobile companies making a play in healthcare or whether they’ll actually survive for a few years and get traction.

But, Hubbub isn’t just another one of the many wellness vendors out there. They’re part of Cambia Health. You’ve probably still never heard of them, but Cambia is Regence which is a BCBS plan operating in Oregon, Idaho, Utah, and some counties in Washington. Additionally, they own and/or invest in lots of companies – e.g., HealthSparq, GNS Healthcare, OmedaRx, and Wellero (plus Hubbub).

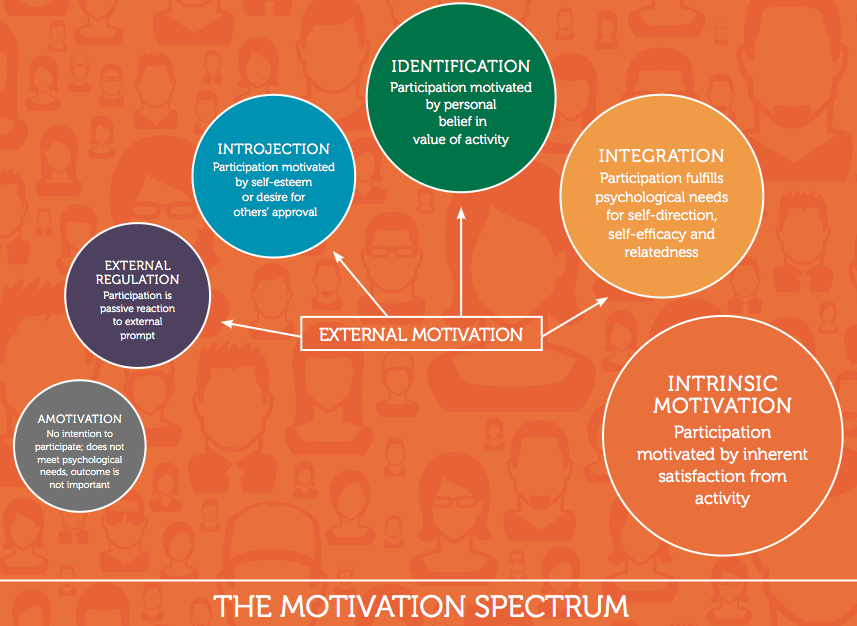

Cognitive Evaluation Theory (CET) concerns intrinsic motivation, motivation that is based on the satisfactions of behaving “for its own sake.” Prototypes of intrinsic motivation are children’s exploration and play, but intrinsic motivation is a lifelong creative wellspring. CET specifically addresses the effects of social contexts on intrinsic motivation, or how factors such as rewards, interpersonal controls, and ego-involvements impact intrinsic motivation and interest. CET highlights the critical roles played by competence and autonomy supports in fostering intrinsic motivation, which is critical in education, arts, sport, and many other domains. (source)

Self-Determination Theory (SDT) represents a broad framework for the study of human motivation and personality. SDT articulates a meta-theory for framing motivational studies, a formal theory that defines intrinsic and varied extrinsic sources of motivation, and a description of the respective roles of intrinsic and types of extrinsic motivation in cognitive and social development and in individual differences. Perhaps more importantly SDT propositions also focus on how social and cultural factors facilitate or undermine people’s sense of volition and initiative, in addition to their well-being and the quality of their performance. Conditions supporting the individual’s experience of autonomy, competence, and relatedness are argued to foster the most volitional and high quality forms of motivation and engagement for activities, including enhanced performance, persistence, and creativity. In addition SDT proposes that the degree to which any of these three psychological needs is unsupported or thwarted within a social context will have a robust detrimental impact on wellness in that setting. (source)

Those are foundational for a lot of the work in healthcare, and I liked this graphic about motivation.

Whether the app works and captures my attention is still TBD. I did download it and register, but I didn’t really get engaged upon registration. And, the website seemed better than the mobile app, but it still had a few issues in terms of how the large top image dominated most of my screen on my laptop.

At the end of the day, their key role like anyone in this space is to figure out how to engage the consumer (or patient or member or individual) as validated in a study they use.

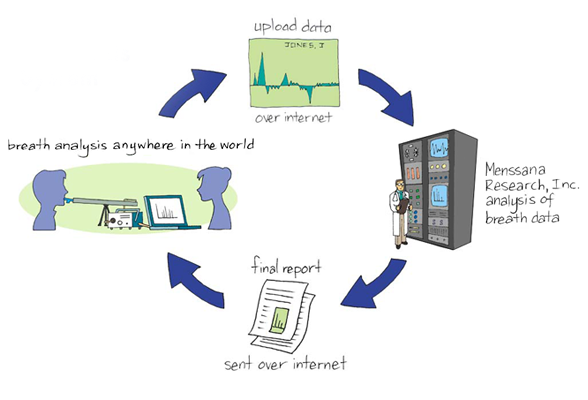

In the spirit of the Internet of Things and the Smart Home, I was intrigued by a short article I read about Menssana Research which can identify 2,000 chemical compounds from our breadth…including signs of cancer and radiation exposure. Pretty cool!

Of course, my mind jumped to the idea of how you could use existing devices (like Nest) which would be tied into our HVAC system and could monitor the overall air in an entire house and look for risks based on the air. (like my idea of the smart toilet) Maybe that’s a little too scary like why an underwriter wants your cell phone data or too much like the Snapshot from Progressive. And, while on the one hand it’s cool, I’m not always sure we’re ready to know things too much in advance so the question would really be how early is the device identifying people and how accurate is it.

As I’m enjoying my time thinking about what’s next, one of the things that I’ve thought a lot about key problem areas in our healthcare system. Obviously obesity is one of them. And, you have lots of companies trying to figure out what to do here.

Build an assessment tool (like Milliman or InterQual) which could be used for assessing patients and creating an evidence-based care plan.

Work with KitchenAid or others to create a branded line of smart devices which used the Internet of Things to do things like re-order healthy foods and suggest menus.

Work with FitBit or other device company and a gamification company to create a kid’s device linked to a game where the key player got fat tied to their activity level and where they opened up new levels tied to their behavior (e.g., eating healthy).

Create online communities for people to share stories and experiences (like PatientsLikeMe but moderated).

Work with Healthways and the Blue Zones effort to create a family centric option tied into the schools and focused on getting everyone healthy across generations.

Create a mobile coach using embodied conversational agents (similar to avatars) to drive behavior change and create a location-based prompts (i.e., as I pull into McDonalds).

Work with manufacturers to create a “beyond the pill” approach to obesity drugs that incorporates coaching and behavior change with the pill being the final mile which should drive greater formulary coverage.

Create a detailed patient journey map based on ethnographic research for weight loss with different triggers and create a “Coach certification” that can be used with coaches to certify that they are following best practices.

Work with biometrics companies (e.g., LabCorp, Quest) or clinics (e.g., MinuteClinic) to create an early identification process for obesity and/or metabolic syndrome with a process for them to “prescribe” a specific program.

Research and design ethnic specific obesity related programs for sub-populations within the US. For example, partner with the large Hispanic groups to create a Spanish (language, experience, culturally relevant) programs.

Partner with the ADA and NKF to jointly address metabolic syndrome together.

Work with a grocery store or food company to create an augmented reality process for smart phones or Google Glass that would highlight healthy foods on the shelf and help people shop better.

Work with Medicaid to create a process by which people earned cell phone minutes or lower copays based on activity and participation.

As the parent of kids, I’m obviously concerned about what they do as they grow up. On the one hand you want them to learn to make decisions. On the other hand, you don’t want to endanger them. That requires helping them to understand right from wrong. That requires helping them to make smart decisions and understand the long-term implications of them.

As someone who has watched people throw away their life on drugs and the son of someone who worked in drug and gang rehabilitation centers, I personally see it as a slippery path. I agree that alcohol may be the gateway “drug” when not used appropriately and can be very dangerous for kids and for many adults who can’t control themselves. You can find lots of research on alcohol related deaths due to increased disease burden or simply drunk driving.

So, like many health related topics, the information out there is very confusing for our kids. On the one hand, we point out what your brain looks like on drugs (if you remember the PSA from the 80s and 90s).

On the other hand, we talk about medical marijuana, and we have states where it’s now legal to buy marijuana like Colorado. But, the idea of walking down the street and seeing cannabis stores is crazy to me.

Perhaps a sad sign of this issue is the spike in travel to Colorado especially around Spring Break. They’ve also seen an enormous jump in applications to go to college in Colorado. (I think I’ll bet on causality not just correlation here.)

At the end of the day, I think we want to keep our kids safe and help them avoid anything addictive – tobacco, drugs, and alcohol. (And, yes…you could take this further to look at caffeine or sugars or other things that impact their health.) At a minimum, we want to help them understand the facts and make sure they know the risks and determine if they fit the addictive profile or not. They already have a hard time navigating childhood and adolescence…let’s be careful not to make it too easy for them to fall off track. Unfortunately, decisions like this have broader implications on our next generation even if they don’t actually use marijuana.

Of course years ago, we used opium, cocaine, and herion as medicine also…but we outgrew that phase of “modern healthcare” so maybe this too will pass.

NOTE: The opinions expressed here are those of the author and are not reviewed in advance by anyone but the individual author. They represent personal opinions not the opinions of any employer.

July 10, 2014

July 10, 2014